Smart Ways to Pay Off Credit Card Debt Faster: Why It Matters Now

Paying off credit cards faster in 2025 isn’t just about feeling less stressed; it’s about buying back your freedom in a world where prices, rents and subscription costs never stop creeping up. If you’re searching how to pay off credit card debt fast, you’re really asking: “How do I stop my past purchases from stealing my future paycheck?” The good news is, there’s nothing magical or mysterious about it. With a few smart habits, clear priorities and some modern tools, you can speed up your payoff timeline much more than you probably expect and keep more of your income for the things you actually care about.

Historical Background: How We Got So Hooked on Plastic

Credit cards took off in the US in the 1950s, when banks realized they could lend quickly, profit from interest and build loyalty at the same time. For decades, the idea was simple: swipe now, worry later. By the 1980s and 1990s, aggressive marketing, airline miles and cash‑back perks normalized carrying a balance; paying interest became a routine expense, not a red flag. After the 2008 crisis, regulators tried to clean up the worst tricks, but the basic model stayed: easy credit plus high rates. In the 2020s, online shopping, buy‑now‑pay‑later apps and contactless payments made spending almost frictionless, while wages grew slowly and many people plugged everyday gaps with plastic.

Basic Principles: How to Stop Feeding the Interest Machine

To use the best ways to pay off credit card debt, you first need to stop adding new debt. That means freezing lifestyle creep, cutting non‑essential recurring charges and using a debit card or cash for anything that isn’t truly urgent. Next, you prioritize interest, not emotion: cards with the highest APR drain you fastest, even if the balance looks modest. Choose a payoff system and stick to it—either the “avalanche” (highest rate first) for maximum math efficiency or the “snowball” (smallest balance first) for faster wins and motivation. Whichever path you pick, the key is consistency and making more than the minimum every single month.

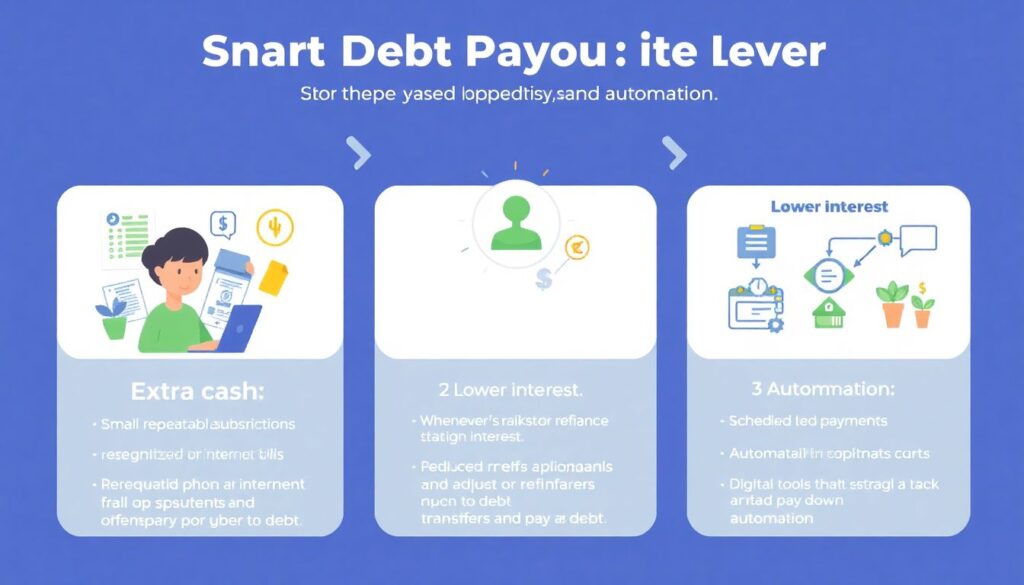

Core Strategies: Turning a Plan into Real Progress

In practice, smart debt payoff relies on three levers: extra cash, lower interest and automation. First, you hunt for small, repeatable savings—cancel underused subscriptions, renegotiate phone or internet bills, redirect raises and tax refunds straight to debt. Second, whenever it’s realistic, you try to lower the cost of borrowing: calling your issuer to request a lower APR, exploring credit card debt consolidation options through a reputable bank or credit union, or checking whether your employer or union offers financial counseling. Third, you lock in your plan with automatic payments on payday, so money hits your card before you can spend it elsewhere.

Modern Tools: Balance Transfers, Consolidation and Relief Programs

Today’s market offers more technical tools than your parents ever had. You can use balance transfer credit cards to pay off debt at a much lower temporary rate—sometimes 0% for 6–18 months—if your credit score allows it and you’re disciplined about paying it down before the promo ends. For larger, scattered balances, a fixed‑rate personal loan can simplify everything into one monthly payment, which is one of the best ways to pay off credit card debt for people who get overwhelmed by multiple due dates. When things are truly out of control, reputable debt relief programs for credit card debt can negotiate lower interest or structured repayment, though they may affect your credit and should be approached carefully.

Examples of How These Strategies Work in Real Life

Imagine you owe on three cards: $900 at 28% APR, $2,500 at 24%, and $4,000 at 19%. Under the avalanche method, you’d pay minimums on the two larger balances and throw every spare dollar at the 28% card until it’s gone, then roll that freed‑up payment to the next card—like a snowball rolling downhill but guided by interest rate. If your monthly budget frees up an extra $250 and you add a temporary 0% transfer for the 19% balance, your payoff timeline can shrink from many years to a couple of focused ones. The math isn’t glamorous, but the compounding effect of higher payments plus lower interest is what really accelerates your progress.

Common Misconceptions That Keep People Stuck

Several myths slow people down. One is thinking, “It’s pointless to pay more than the minimum, I’ll never get out.” In reality, even small increases—an extra 10–15% of the minimum—can shave months or years off your payoff. Another misconception is that consolidation is always a scam; in truth, credit card debt consolidation options can be extremely helpful when the new loan’s interest rate and fees are clearly lower and you stop using the old cards for new spending. Finally, people often assume their credit score will be ruined if they seek help, but ignoring late payments or maxed‑out cards does far more damage than using structured solutions early.

Staying Motivated and Avoiding the Debt Trap Again

Once your balances start shrinking, it’s tempting to relax and slide back into old habits. Instead, treat each paid‑off card as a chance to permanently adjust your lifestyle: keep your expenses at the “debt payoff” level for a few extra months and build an emergency fund, so the next car repair or medical bill doesn’t go straight back on plastic. Use your card as a tool—pay in full every month and enjoy the protections and rewards—rather than a safety net. Paying off credit cards fast is less about one dramatic move and more about a series of steady, deliberate choices that, over time, completely change your financial trajectory.