The Fundamentals of Personal Finance for Busy Professionals

Why money feels harder when your calendar is full

You’d think that once you start earning a solid income, money stress should disappear. Yet many busy professionals hit six figures and still feel like they’re running on a treadmill: good salary, nice title, zero peace of mind. The problem usually isn’t intelligence or discipline. It’s that personal finance was never designed with a 60‑hour workweek and constant context switching in mind.

So instead of more guilt or abstract theory, let’s break down the fundamentals of personal finance for busy professionals in a way that fits a crowded schedule — with real‑world cases and simple systems.

—

A brief (and useful) history of personal finance

From “don’t go into debt” to complex financial lives

For most of the 20th century, personal finance advice could be summed up in a sentence: get a steady job, don’t take on too much debt, buy a house, retire with a pension. That worked in a world where people spent decades in one company, mortgages were simple, and pensions were the norm.

Things changed fast:

– 1970–1980s: Pensions began to disappear. Retirement shifted from “your employer will handle it” to “you’re on your own.” In the U.S., 401(k) plans appeared; in other countries — different flavors of self‑directed retirement accounts.

– 1990–2000s: Cheap credit and credit cards became everywhere. Financial products got more complicated, but financial education didn’t keep up.

– 2010–today: Income for many professionals grew, but so did lifestyle expectations — global travel, subscriptions for everything, private schools, tech gadgets. At the same time, you’re expected to be your own pension manager, tax planner, and investment strategist.

That’s why a modern *personal finance for professionals course* looks nothing like what your grandparents needed. Your money life is more complex and your time is more limited, so your systems need to be simpler and more automated.

—

Core principles: the 20% you must get right

The 4 pillars of solid personal finance

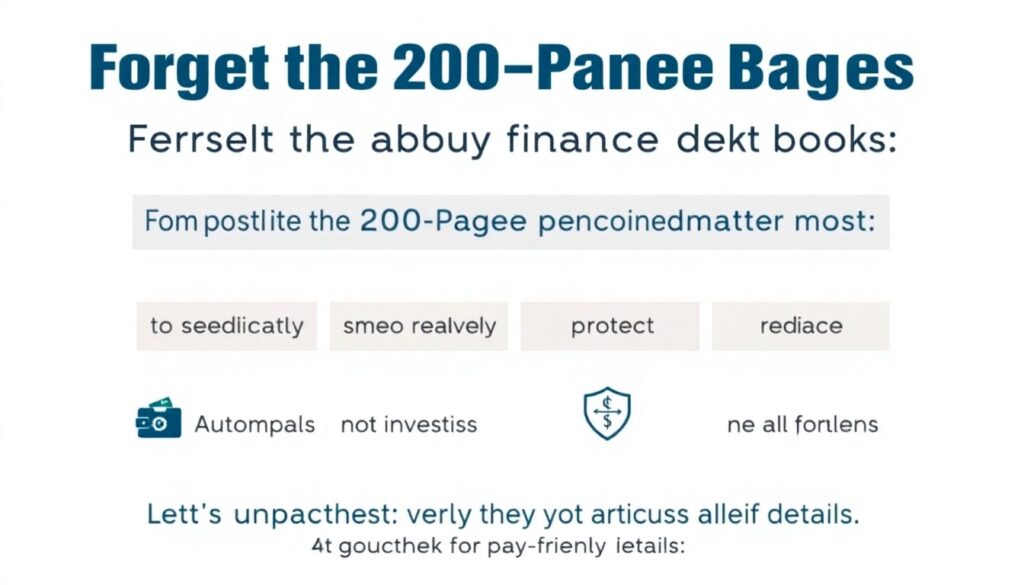

Forget the 200‑page finance books. For a busy professional, four pillars matter most:

1. Spend deliberately, not reactively

2. Automate saving and investing

3. Protect against bad surprises

4. Align money with your actual life plans

Let’s unpack these, with practice‑friendly details.

—

1. Spend deliberately (not perfectly)

Most advice talks about “cutting lattes.” For high‑earning, time‑poor people, that’s the wrong focus. The real problem is unconscious spending: money leaking into things you don’t truly value simply because you’re tired or too busy to decide.

Long paragraph:

Instead of tracking every cent, define 3–4 *big rocks*: housing, transport, kids/education, and lifestyle (restaurants, subscriptions, travel). If those are aligned with your priorities and are within reasonable percentages of your income, you can stop obsessing over minor details. A surgeon I coached was beating herself up over food delivery costs. Turned out her grocery + delivery spending was under 8% of her income. The real drain was an oversized house she barely used and a second car she didn’t need. Adjusting those two decisions freed up more than $2,000 a month — way more than cutting takeout ever could.

Short paragraph:

In other words: fix the big things first; the rest is background noise.

—

2. Automate saving and investing

If your money plan requires weekly willpower, it will fail. You’re already making dozens of important decisions at work. By the time you get to your personal finances, your decision‑making muscle is exhausted.

Here’s a simple automation stack many *financial planning services for busy professionals* quietly build for their clients — you can copy the logic yourself:

1. Paycheck hits account.

2. Automatic transfers move fixed percentages to:

– Retirement/investment accounts

– Emergency fund / short‑term goals

– Separate “fun money” account

3. Bills and debt payments are on autopay from the main account.

4. Whatever remains is guilt‑free spending.

No heroic discipline, no constant tracking — just a pipeline. This is where the *best personal finance apps for professionals* help: they can categorize spending for you, send simple summaries, and nudge you when something looks off, instead of you living inside spreadsheets.

—

3. Protect against bad surprises

Wealth isn’t only about how much you earn or invest. It’s also about how much you *don’t lose* when life goes sideways: job loss, illness, divorce, a lawsuit, or a failed business.

Short paragraph:

Protection is boring until the day it’s the only thing keeping you from financial disaster.

Longer paragraph with case:

Consider Mark, a 38‑year‑old IT project manager. Great income, two kids, a mortgage. He assumed his employer disability insurance was “probably enough.” It wasn’t. When a back injury took him out of traditional office work for almost a year, he discovered his policy only covered a portion of his base salary — no bonuses, no stock grants. His cash flow went from comfortable to negative almost overnight. Only after scrambling to refinance debt and cut expenses did he speak to a planner, who helped him calculate what *true* coverage would have looked like. If he had spent one afternoon earlier in his career understanding his insurance, he could’ve avoided months of financial stress.

—

4. Align money with your actual life plans

If your finances aren’t anchored to concrete goals, they’ll drift. “Save more” and “invest better” sound nice, but they don’t guide real‑world decisions.

Short paragraph:

Tie numbers to dates and events: “We want to be able to take 3 months off in 5 years,” or “We want the option for one parent to go part‑time when our child is 3.”

Case:

A corporate lawyer couple I worked with felt trapped. They thought their only choices were: keep grinding 70‑hour weeks for another 20 years, or burn everything down and move to a farm. When we mapped their cash flow, stock compensation, and projected savings, we discovered a third option: maintain the current grind for 5 years, aggressively invest surplus cash, then intentionally downshift to lower‑pay but lighter‑stress roles. Once their money plan matched a specific timeline, it became far easier to say “no” to lifestyle creep and “yes” to investing more.

—

Real‑world cases: how busy professionals actually apply this

Case 1: The 33‑year‑old doctor with “good income, zero plan”

Emma, a medical specialist, earned well into six figures. Still, her bank balance felt like a roller coaster: some months she was flush, other months she dipped into overdraft. Her pattern:

– No system for quarterly tax payments

– Random investing into whatever funds colleagues mentioned

– Credit card paid “whenever I remember”

We spent one 90‑minute session (this could just as easily have been via a *hire personal financial advisor online* platform) to build a simple structure:

– 25% of every paycheck auto‑transferred to a “tax + investments” account

– A fixed monthly contribution into a globally diversified index fund portfolio

– All high‑interest debt targeted with a clear payoff schedule

– A capped “guilt‑free” spending amount each month

Within 6 months, her credit card was paid off, she had 3 months of living expenses saved, and investing became something that just “happened in the background.” The biggest shift wasn’t mathematical; it was psychological. She stopped feeling behind, which freed up mental energy for her actual work.

—

Case 2: High‑income executive, high‑stress relationship with money

Alex, 45, was a senior executive earning a very high income. On paper, he looked wealthy: bonuses, stock options, nice house. In reality:

– Most of his net worth was tied to his employer’s stock

– His expenses scaled every time his bonus went up

– He had no clear exit plan if he burned out or was laid off

We reframed his situation around *investment strategies for high income professionals* that focus on de‑risking:

1. Gradually diversify out of company stock into low‑cost index funds and some bonds.

2. Cap lifestyle inflation: every bonus was split — 50% to long‑term investments, 30% to specific goals (kids’ education, mortgage prepayment), 20% to lifestyle upgrades.

3. Build a 12‑month “freedom fund” to allow a potential career pivot without panic.

Three years later, Alex took a lower‑paid but far more satisfying role at a smaller firm. Thanks to his diversification and freedom fund, that decision was based on values, not fear.

—

Case 3: Dual‑career couple and the decision to outsource

Priya (product manager) and Daniel (consultant) had two kids and almost no free time. They tried DIY money management for years: spreadsheets, podcasts, books. Nothing stuck. Not because they were incapable — they were simply exhausted.

Instead of more self‑help, they decided to pay for structured *financial planning services for busy professionals*. Their planner:

– Consolidated old retirement accounts

– Created a joint investment plan

– Optimized their insurance and estate documents

– Set up automatic transfers and bill payments

The key insight: for them, “buying back time and mental space” was worth far more than the planner’s fee. Could they have figured everything out alone? Probably. Would they have actually done it without outside accountability? Very unlikely.

—

Common misconceptions that cost professionals money

Myth 1: “I make good money, so I don’t need to worry (yet)”

High income can hide bad habits — for a while. The danger is that when a shock hits (job loss, industry shift, health issue), the lifestyle you built on a fragile foundation becomes a trap. A strong income is an opportunity, not a guarantee. Use the good years to build resilience, not just bigger monthly payments.

—

Myth 2: “Personal finance is too complicated — I’ll deal with it later”

The industry loves jargon. But your personal setup doesn’t have to be complex. In fact, complexity is usually the enemy of consistency.

Short paragraph:

You don’t need to become your own CFA. You need a handful of clear decisions: how much to save, where to invest (usually broad index funds), how to protect yourself (insurance, legal basics), and how to avoid lifestyle bloat.

If you truly hate this stuff, consider options like a *personal finance for professionals course* that’s built for non‑experts or simply *hire personal financial advisor online* for a flat‑fee review once a year. One afternoon of focused attention can fix years of drift.

—

Myth 3: “More apps = better control”

Tech can help, but it’s not magic. Many professionals download five apps, connect all their accounts, and then… never open them again.

Short paragraph:

Pick one of the *best personal finance apps for professionals* that does three things well: automatic categorization, easy recurring transfers, and simple goal tracking. Use it to implement your system — not to stare at charts.

—

Myth 4: “Investing is about picking winners”

Busy professionals often think they’re supposed to research individual stocks, follow macro news, and “beat the market.” That’s a full‑time job — and even most full‑timers don’t reliably succeed.

Short paragraph:

For 90% of people, the winning move is boring: broad diversification, low fees, consistent contributions, and staying invested through market noise.

Longer paragraph:

In practice, that might mean a mix of global stock index funds and some bond funds appropriate for your risk tolerance and time horizon. Rebalance once or twice a year. That’s it. The exciting part of your financial life should be what money allows you to do, not the adrenaline rush of guessing which company’s stock will pop next.

—

Putting it all together (in a way you’ll actually follow)

A simple 5‑step starter plan for busy professionals

1. Get a 1‑page overview.

List your accounts, debts, assets, and monthly fixed expenses. If it doesn’t fit on one page, simplify the structure (fewer accounts, consolidated investments).

2. Decide your automation rules.

Choose percentages for: retirement/investing, emergency fund, and “fun money.” Set automatic transfers once per paycheck.

3. Check your protection.

Review insurance (health, disability, life, liability) and basic legal docs (will, beneficiaries, powers of attorney). Fix obvious gaps.

4. Pick your tools.

Choose one app for tracking and automation. Don’t chase features; prioritize clarity and ease of use.

5. Schedule a 90‑minute “money strategy” session once a year.

This can be solo, with your partner, or with a planner. Review goals, net worth, and whether your money is still aligned with your actual life.

—

Final thought

You don’t need a perfect financial plan; you need a good‑enough system you’ll actually stick to on your busiest weeks. When you treat money like any other important project — clear goals, simple processes, occasional reviews — the fundamentals of personal finance for busy professionals stop being an endless to‑do item and start becoming a quiet engine in the background of your life.