Why a Cash Cushion Got More Interesting in 2025

For the first time in over a decade, cash actually *pays* you to hold it. After the global rate-hike cycle of 2022–2024, yields on safe instruments jumped from basically zero to levels that, in real terms, rival conservative bond portfolios. That changes how you should think about your emergency fund and short‑term goals: your “just in case” money can now be a meaningful, interest‑bearing asset instead of dead weight in a checking account.

How Much Cash Cushion Makes Sense Now?

Most financial planners still land in the same basic range: 3–6 months of essential expenses for a stable W‑2 earner, 6–12+ months for freelancers, business owners, or those with volatile income. What changed by 2025 is not the *amount* of cash you need, but the opportunity cost of where you keep it.

In the low‑rate years (roughly 2009–2021), holding a big cash buffer meant guaranteed erosion from inflation. By 2023–2024, high‑yield vehicles were paying several percentage points more than traditional savings, and even as rates fluctuate in 2025, the spread between “lazy cash” and “optimized cash” is still massive. Keeping your cushion in a 0.01% account is no longer just sub‑optimal; it’s a measurable drag on your household balance sheet.

—

Modern Cash Stack: Layers, Not Just One Account

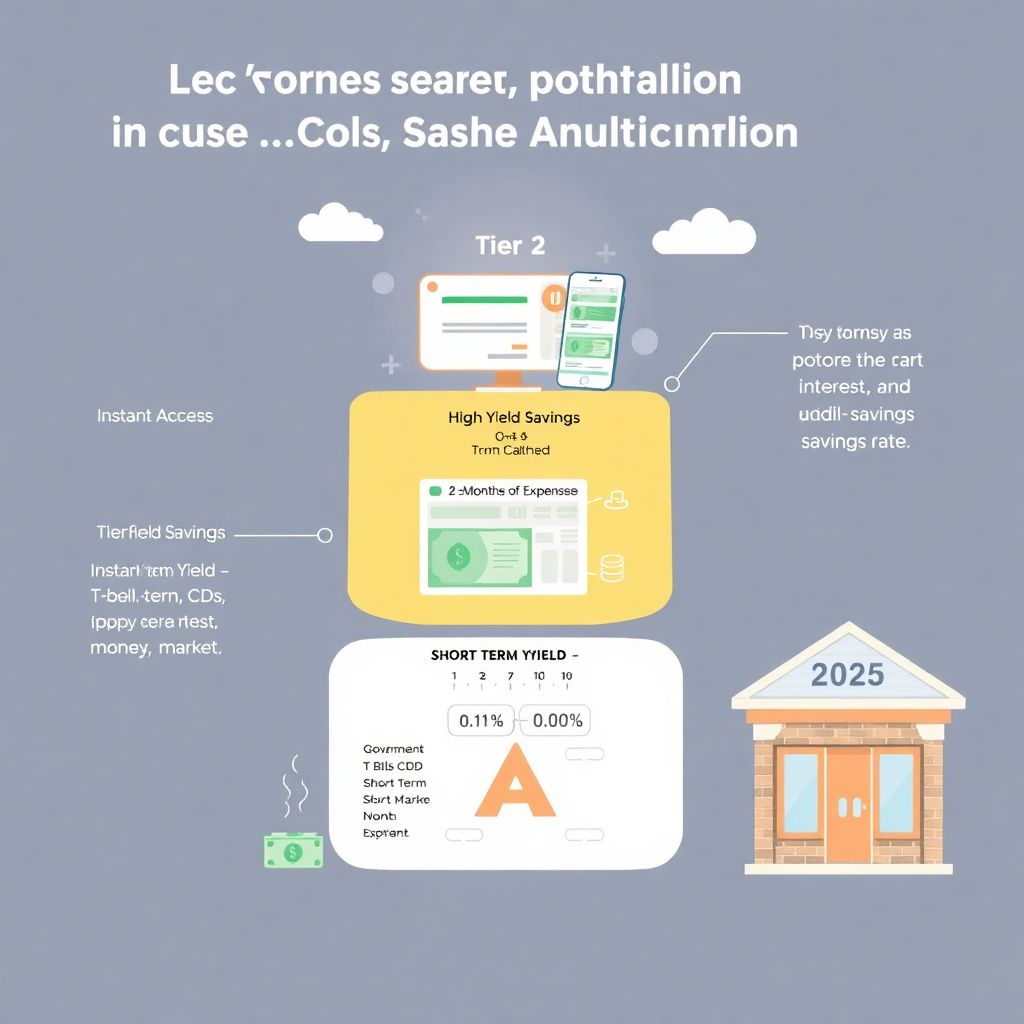

Tiered Structure: Liquidity First, Yield Second

A smart 2025 strategy is to treat your cash like a mini capital structure: different “tranches” with different liquidity and return characteristics.

– Tier 1 – Instant access (0–1 month of expenses)

Ultra‑liquid checking or a highly liquid savings account linked to your debit card for immediate access.

– Tier 2 – High‑yield liquid (2–5 months of expenses)

High‑yield online savings or the best money market accounts for emergency fund purposes, where you can transfer funds within 1–2 days.

– Tier 3 – Short‑term yield enhancement (optional)

Treasury bills, short‑term CDs or cash management accounts where you accept a bit of friction or minimal lockup in exchange for higher yield.

This layered approach keeps your true “emergency” money frictionless while still letting most of your cushion earn competitive returns.

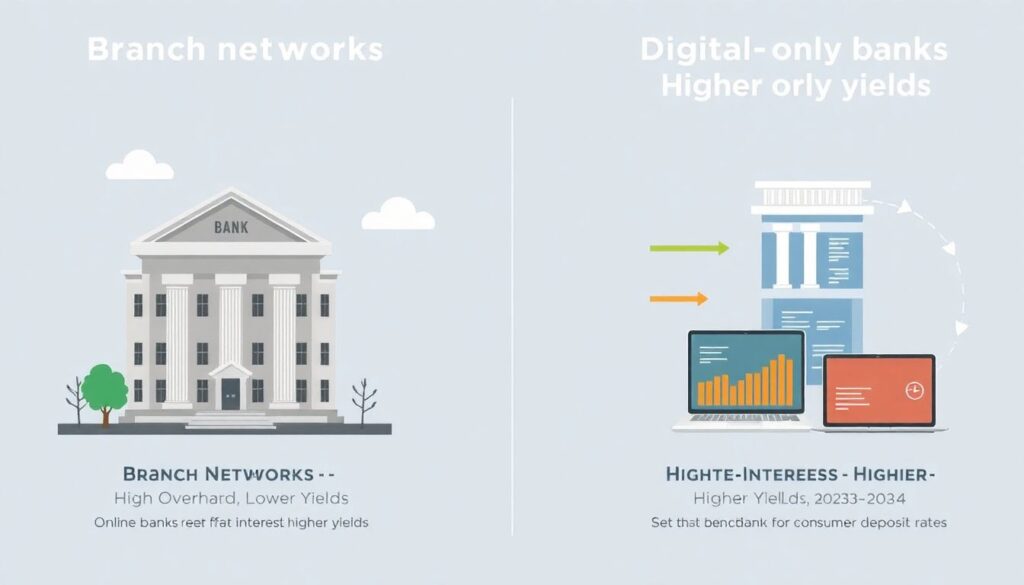

Why Online Banks Dominate the Cash Game

Branch networks are expensive. Digital‑only banks don’t carry that overhead, and in 2023–2024 they systematically offered higher yields than legacy institutions. That pattern still largely holds: online banks with highest interest on savings tend to set the benchmark for consumer deposit rates, and traditional banks adjust slowly or only for select clients.

In practice, that means your local branch may be paying a fraction of what a regulated online bank offers on the same insured product. The technological stack—API‑driven core banking, real‑time payments rails, and scalable cloud infrastructure—lets online players profitably pass more of the interest spread back to you.

—

Understanding Today’s Interest Landscape

From Zero Rate World to Income‑Generating Cash

Between the global financial crisis and the pandemic, policy rates hovered near zero in many developed markets. According to FDIC and Bank of England data, average savings account yields in major economies were often below 0.1% for years. Then inflation spiked, central banks tightened aggressively, and by 2023–2024 policy rates climbed to multi‑decade highs.

The result:

– High‑yield savings, money market funds, and T‑bills started yielding several percentage points annually.

– Corporate and fintech cash products emerged with institutional‑style sweep programs, automatically moving idle client balances into money market instruments.

Even with potential rate cuts in 2025–2026, the structural shift is clear: regulators, banks, and consumers have re‑priced the value of cash. The historical assumption that “cash pays nothing” is no longer safe.

Key Factors Driving high yield savings account interest rates

Short‑term yields now react quickly to macro conditions. For your cash cushion, the main drivers are:

– Central bank policy rates – The floor for risk‑free yields; cuts or hikes ripple through every money market product.

– Bank funding needs – When banks want deposits, they raise rates on savings and CDs; when they’re flush, they quietly reduce offers.

– Competition from money market funds and T‑bills – If retail can easily buy government paper at attractive yields, banks must respond or see deposits leave.

– Fintech innovation – Aggregator apps can move consumer balances programmatically to higher‑yield banks, increasing rate sensitivity and transparency.

For you, this means yields can adjust noticeably within months. A “set and forget” mentality for your savings account is no longer optimal; periodic rate checks are now part of basic financial hygiene.

—

Where to Park Cash for Short Term High Interest

Priority 1: Safety and Liquidity

An emergency fund isn’t a speculative asset. The hierarchy is:

1) Capital preservation

2) Liquidity

3) Return

So when you ask where to park cash for short term high interest, what you’re *really* optimizing is the best rate you can get *after* you lock in those first two priorities. That generally points to:

– Insured high‑yield savings accounts

– Money market accounts at reputable banks or credit unions

– Government‑only money market funds

– Short‑term government securities (like T‑bills in the U.S.)

These are instruments where default risk is extremely low, market volatility is limited, and access is either same‑day or within a few days.

Savings Accounts vs Money Market Accounts vs Cash Funds

Short answer: they run on similar economic engines but with different regulatory wrappers and user experiences.

– High‑yield savings accounts

Simple, FDIC/NCUA‑insured (or equivalent), variable rate. Ideal as the “hub” of your cash strategy.

– Money market accounts (bank products)

Also typically insured, may offer limited check‑writing or debit access. The best money market accounts for emergency fund goals combine near‑savings‑account liquidity with slightly better yields and some transactional features.

– Money market funds (investment products)

Not deposits, but diversified portfolios of short‑term instruments. They aim for stable value and daily liquidity, but they’re technically investments subject to market risk and different regulations.

By 2025, user‑facing apps increasingly blur these distinctions, but under the hood, the regulatory category still dictates insurance coverage, allowable assets, and risk profile.

—

Best Short Term Investment Options for Cash Reserves

T‑Bills and Short‑Term Governments

For many savers, short‑term government bills are now the baseline for evaluating yield. They’re directly tied to monetary policy, backed by the sovereign, and have clearly defined maturities.

Advantages:

– Transparent pricing and yields

– Minimal credit risk for stable governments

– Ability to ladder maturities (e.g., 4, 8, 13 weeks) to balance liquidity and return

The downside: you may accept a small lockup until maturity unless you sell on the secondary market, and there can be minor price drift with rate changes.

CDs and Term Deposits as Yield Enhancers

Certificates of deposit (or term deposits) are another piece of the puzzle. When rate curves are favorable, locking in a 6–12 month CD on a portion of your cushion can be rational, especially if you don’t foresee needing *all* of that cash at once.

Smart use case in 2025:

– Keep 1–2 months fully liquid

– Put a portion (say 3–6 months) into a ladder of short‑term CDs

– Accept modest early withdrawal penalties as a form of “liquidity insurance fee”

You’re effectively converting part of your emergency fund into quasi‑bond exposure, but with clear terms and bank insurance up to regulatory limits.

—

How Much Yield Is “Enough” for a Cash Cushion?

Balancing Rate Chasing with Friction Costs

There’s a behavioral trap here: constantly opening new accounts to chase a 0.10% difference can waste time and increase cognitive overhead. Think in *expected value* terms.

Ask:

– What’s the incremental interest from switching, net of any temporary transfer delays?

– How likely are you to stick with the new provider long enough to realize the benefit?

– Does managing multiple platforms create risk of errors or missed bills?

A practical 2025 guideline is to react when the spread is material—say, when your current yield is more than 1–1.5 percentage points below competitive offers for similar risk. At that point, the extra income justifies the administrative effort for most households.

Automation: The Quiet Edge

Modern fintech tools turn optimization into a background process. Many apps can:

– Auto‑sweep checking surpluses into high‑yield accounts

– Alert you when your bank’s rate drops relative to peers

– Set target balances for “instant access” vs “yield” buckets

In effect, you’re building a rules‑based cash management system that adjusts for you. This is how institutions have treated cash for decades; 2025 consumer‑grade tools finally make that approach accessible at small balances.

—

Macroeconomic and Industry Implications

The Economics of Deposits Have Shifted

At a macro level, higher short‑term rates changed the calculus for both banks and households:

– Households are increasingly yield‑sensitive: they move cash quickly when rates diverge, especially younger, app‑native demographics.

– Banks face compressed net interest margins if they don’t reprice deposits competitively but still hold higher‑yield assets.

– Fintechs and brokerages use attractive cash yields as customer acquisition and retention tools, sometimes running near‑break‑even on cash to profit from other services.

This re‑pricing of cash introduces more dynamic flows between traditional banks, online challengers, and capital markets. Your decision about where to stash your emergency fund now has a non‑trivial aggregate effect on funding costs across the system.

Forecasts: What 2025–2030 Might Look Like

No one can forecast interest rates with precision, but some structural trends are visible:

– The probability of a *permanent* return to 0% policy rates looks lower than a few years ago. Post‑pandemic inflation and fiscal dynamics reshaped central bank reaction functions.

– Retail access to institutional‑grade products will likely continue expanding. Expect smoother on‑ramps from your phone into T‑bills, repo‑backed funds, and other low‑duration vehicles.

– Deposit “stickiness” is declining. As UX improves and account opening friction falls, switching providers for better yields becomes almost costless.

For individual savers, that means the notion of a single, static “savings account” will gradually be replaced by a portfolio of integrated cash tools under one interface—even if, behind the scenes, those tools spread deposits across multiple institutions and products.

—

Practical 2025 Playbook: Building Your Interest‑Bearing Cushion

Step‑by‑Step Setup

Here’s a streamlined way to execute all of this without turning it into a part‑time job:

1. Define your target cushion size

Calculate core monthly expenses, pick a 3–12‑month target based on job security and risk tolerance.

2. Choose a main high‑yield hub

Select one of the online banks with highest interest on savings that offers:

– Solid regulatory protections

– Clean mobile app and fast transfers

– No or low maintenance fees

3. Segment liquidity needs

– Keep 1 month in checking for bills + card spending.

– Move the rest into your high‑yield hub as Tier 2.

4. Optionally add a Tier 3 layer

Once Tier 2 is funded, consider moving a slice into:

– Short‑term T‑bills via your brokerage

– A CD ladder matched to your risk tolerance

5. Automate contributions and reviews

– Set up monthly auto‑transfers into your hub.

– Put a recurring calendar reminder every 6–12 months to review your yields versus market leaders.

Picking the Right Mix for Your Situation

The best short term investment options for cash reserves depend heavily on your personal volatility—of both income and expenses. A freelancer with lumpy revenue may keep almost everything in instantly redeemable accounts, sacrificing some yield for peace of mind. A dual‑income household with stable jobs might lean more aggressively into CDs and T‑bill ladders, knowing they’re unlikely to tap the deepest layer of their cushion.

The key is consistency: once you design a structure that matches your risk profile, automate it and resist tinkering based on short‑term rate headlines.

—

Bottom Line: Cash Is No Longer an Afterthought

By 2025, ignoring yield on your emergency fund is effectively leaving easy money on the table. The spread between legacy savings accounts and optimized products is now large enough to matter over surprisingly short timeframes, and the frictions to upgrade are the lowest they’ve ever been.

Treat your cash cushion as a deliberate, interest‑bearing component of your financial plan. Use a layered structure, lean on modern tools, and keep an eye on evolving high yield savings account interest rates—but only adjust when the math is clearly in your favor. Done right, your “safety net” quietly transforms into a compact, low‑risk income engine that works for you even when you’re not thinking about it.