Most people don’t get rich because they run out of money.

They get stuck because every raise quietly turns into a nicer lifestyle instead of real wealth.

Below is a practical, conversational guide on how to avoid lifestyle inflation and grow wealth without feeling like you’re punishing yourself.

—

What Lifestyle Inflation Really Is (And Why It Sneaks Up on You)

Clear definition in simple words

Lifestyle inflation is what happens when your spending grows automatically every time your income grows. You get a raise, bonus, promotion, new job — and instead of your bank balance rising, your standard of living rises:

– bigger apartment instead of same rent

– new car instead of keeping the old one

– more dinners out instead of cooking a bit more

In other words: *your life gets “nicer”, but your net worth barely moves*.

A useful way to picture it:

> Income ↑ → Lifestyle ↑ just as fast → Wealth = flat

If you want to understand how to avoid lifestyle inflation, the key is to deliberately *break* this automatic link between higher income and higher day‑to‑day spending.

—

Why Lifestyle Inflation Blocks Wealth (With Fresh Numbers)

What the data says (2022–2024)

Even as incomes have risen recently, many households are not getting ahead:

– According to the U.S. Bureau of Economic Analysis, the personal saving rate averaged *around 3.5% in 2022* and only slightly higher at *about 4% in 2023*, well below the decade before the pandemic. Through mid‑2024 it hovered roughly in the 3–4% range again, meaning most people are saving only a few cents from every dollar they earn.

– The New York Fed reports that credit card balances hit about $986 billion in Q4 2022, then around $1.13 trillion by Q4 2023, and stayed over $1.1 trillion through mid‑2024. That’s a clear sign that a big share of higher prices and upgraded lifestyles is being financed by debt, not by growing savings.

These numbers show a pattern: incomes can go up, but if lifestyle goes up just as fast — or faster — debt and stress grow, not wealth.

—

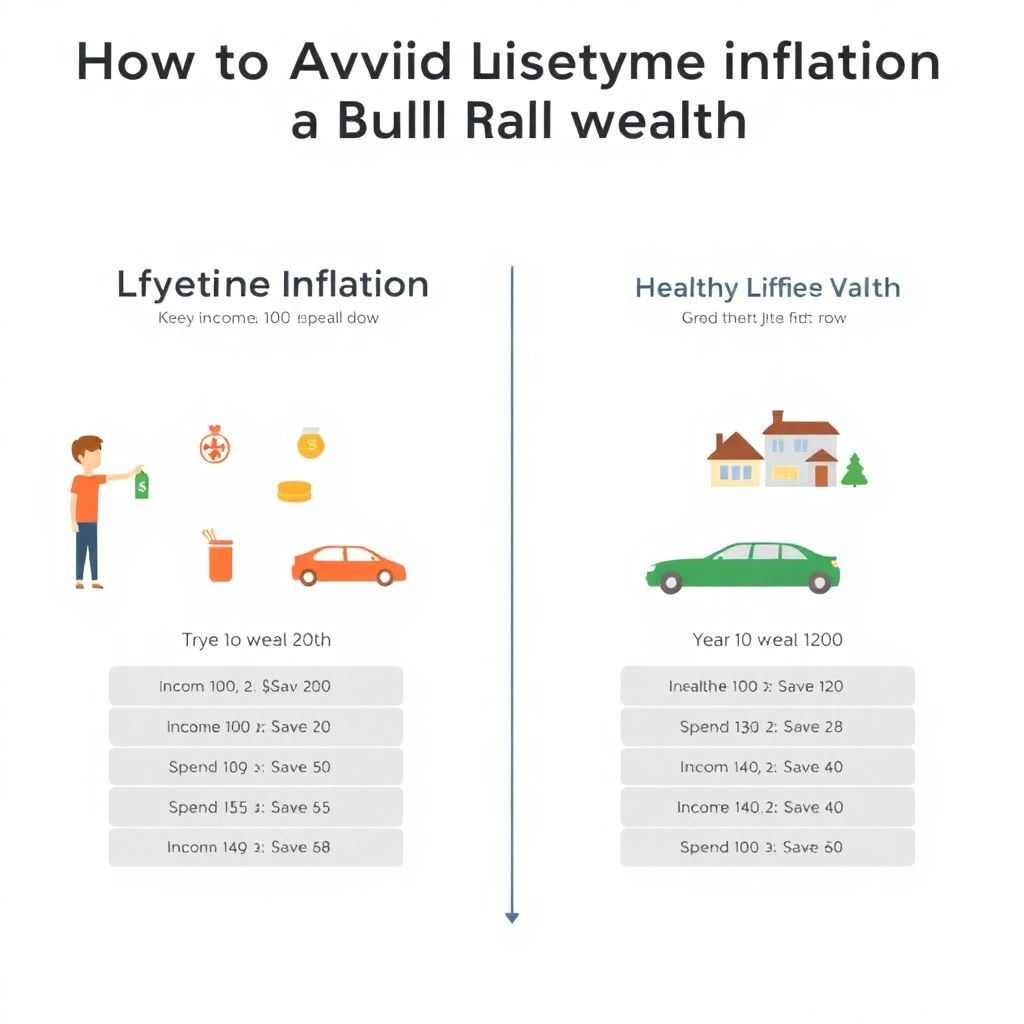

Lifestyle Inflation vs. Healthy Lifestyle Growth

A comparison that actually matters

Not all lifestyle upgrades are bad. The problem isn’t spending more money; it’s *how* and *why* you spend more.

Think in terms of two paths:

1. Lifestyle Inflation Path

– You match coworkers’ cars, phones, and vacations.

– Raise = higher fixed bills (rent, car payment, subscriptions).

– Almost no change in savings or investing.

2. Healthy Lifestyle Growth Path

– You improve comfort and joy *after* you lock in savings goals.

– Raise = higher investing rate first, small lifestyle bump second.

– Net worth grows each year, lifestyle improves slower but safer.

A simple text diagram to visualize it:

– Inflation path

– Year 1: Income 100 → Spend 95 → Save 5

– Year 2: Income 120 → Spend 114 → Save 6

– Year 3: Income 140 → Spend 133 → Save 7

– Healthy growth path

– Year 1: Income 100 → Spend 85 → Save 15

– Year 2: Income 120 → Spend 92 → Save 28

– Year 3: Income 140 → Spend 100 → Save 40

Both people “feel” better off. But only the second is actually building real freedom.

—

Core Principles: How to Avoid Lifestyle Inflation in Real Life

Principle 1: Decide your lifestyle first, not after each raise

Instead of letting your lifestyle creep up randomly, you set a target lifestyle level that’s comfortable and sustainable *for the next few years*, then stick to it even when income rises.

Think of your lifestyle as a “spending ceiling”:

> Income grows → Ceiling stays mostly the same → Gap becomes savings/investments

This feels weird at first, because most people are used to income and lifestyle moving together. But once you see your savings rate jump, it quickly becomes motivating.

Principle 2: Automate the “gap” between income and lifestyle

The most practical of all personal finance tips to grow wealth is to automate the gap:

– Decide your current comfortable monthly spending.

– When your income rises, increase your automatic transfer to savings/investments *before* you see the new paycheck hit your spending account.

– You only “see” what’s left – so you don’t feel like you’ve lost anything.

Automation turns willpower into a system. You don’t need to say “no” 50 times a month; you just build a setup where “no” is the default and “yes” is a deliberate, occasional choice.

—

Defining the Key Terms (So We Talk About the Same Thing)

Lifestyle inflation vs. cost-of-living increases

– Cost-of-living increase: Spending more because prices went up, but your lifestyle is unchanged (same apartment, same groceries, same phone plan, but all more expensive).

– Lifestyle inflation: Spending more because your expectations went up (nicer apartment, more expensive restaurants, premium services you didn’t use before).

They often get mixed together. To stay honest with yourself, regularly ask:

> “Did this expense go up because of *prices* or because of *choices*?”

Savings rate, net worth and real wealth

– Savings rate – the percentage of your income you don’t spend. If you earn $4,000 and save $800, your savings rate is 20%.

– Net worth – everything you own (cash, investments, home equity) minus everything you owe (loans, credit cards).

– Wealth – not just a big number; it’s the ability to choose how you spend your time because your net worth supports your life.

When people talk about ways to build wealth on a budget, they’re really talking about increasing savings rate *without* feeling miserable, and then directing that savings into assets that grow.

—

Simple “Diagrams” You Can Picture in Your Head

Income, spending, and wealth as three pipes

Imagine three pipes in a row:

> Income → Spending → Wealth

– If the “spending” pipe is just as wide as “income”, nothing flows to “wealth”.

– You want to consciously pinch the spending pipe so that more automatically flows into the wealth pipe.

In text form:

– Pipe A (income) = wide and growing.

– Pipe B (spending) = intentionally capped.

– Pipe C (wealth) = grows as the difference collects and compounds.

Lifestyle upgrades: small valves, not a fire hose

Picture small valves for upgrades:

– Valve 1: Housing upgrade

– Valve 2: Car upgrade

– Valve 3: Travel upgrade

Healthy behavior:

> You only open *one* small valve at a time, and only after you’ve increased your savings valve first.

—

Practical Tactics to Block Lifestyle Creep

Tactic 1: Use “Raise Rules” for every income jump

Before you get your next raise, promotion, or new job offer, set a simple rule for yourself, such as:

– “Whenever my income goes up, I will put 50–80% of the increase into savings or investments automatically.”

Example: You go from $3,000 to $3,500 per month after tax – that’s a $500 increase.

Your rule: 70% of every raise goes to wealth-building.

– $350 → automatic investments/savings

– $150 → allowed lifestyle bump

You still feel the win, but most of the benefit goes to future you.

Tactic 2: Freeze lifestyle for 1–2 years

Pick a time window (12–24 months) where you commit to:

– No major housing upgrade

– No new car unless the old one dies

– No new subscription unless you cancel a similar one

During this period, let your income grow, but keep your typical monthly spending roughly level. That gap is your rocket fuel.

Tactic 3: Beware “permanent” upgrades

The most dangerous kind of lifestyle inflation is the kind that becomes a *fixed* cost:

– rent and mortgages

– car loans

– private schools

– subscription bundles that add up quietly

Once you inflate these, it’s much harder to go back. Be extremely cautious with decisions that permanently raise your base cost of living.

—

Smart Spending vs. Mindless Upgrading

Compare wants, needs, and “fake needs”

It helps to label your expenses:

– Needs – essentials: modest housing, food, transport, basic healthcare.

– True wants – things that bring you real lasting joy or convenience.

– Fake needs – status purchases, impulse upgrades, boredom spending.

Lifestyle inflation lives almost entirely in “fake needs”.

When deciding on a purchase, ask:

1. “Will this still matter to me in 6–12 months?”

2. “Is there a cheaper version that gives me 80–90% of the benefit?”

3. “If my income dropped 20% tomorrow, would I regret this fixed cost?”

This quick filter alone can stop a lot of unnecessary lifestyle upgrades.

—

From Extra Cash to Real Wealth: Saving and Investing

Why saving is not enough

Parking all your money in cash is safer than overspending, but it’s not how to save money and invest wisely. With inflation still present in 2022–2024, idle cash slowly loses purchasing power.

To grow wealth, you need three layers:

1. Emergency fund – 3–6 months of essential expenses in a simple savings account for surprises.

2. Short‑term goals – money you’ll need in 1–5 years (car, education, relocation). Keep it relatively safe.

3. Long‑term investments – money you won’t touch for 10+ years. Here is where you use stock index funds, retirement accounts, or diversified portfolios.

Why investing early matters (even with small amounts)

A basic text diagram of compounding:

– Year 1: Put in $100 → 7% growth = $107

– Year 2: $107 → 7% = $114.49

– Year 3: $114.49 → 7% = $122.51

The trick is that each year, growth happens not just on your money, but also on previous growth. Over 10–20 years, this snowball effect becomes huge, especially if you keep adding new savings.

—

Concrete, Low-Stress Ways to Build Wealth on a Budget

You don’t need a six‑figure income to start. You need consistency and boundaries.

Start with micro-upgrades to your money setup

– Set one automatic transfer the day after payday into a separate “wealth” account.

– Round up every purchase and move the round‑up to savings or investments.

– Schedule a 30‑minute “money check‑in” once a month to review goals.

Then target the big three spending categories

For most people, the majority of lifestyle inflation hides in:

– Housing – more space, nicer area, fancy amenities.

– Transport – newer car, more debt, higher insurance.

– Food & going out – frequent restaurants, delivery, casual luxuries.

Pulling back just 10–20% in these three areas often frees up more cash than cutting dozens of tiny expenses.

—

Example: Two Friends, Same Income, Different Future

Imagine two people, Alex and Sam, each earning $50,000 after tax in 2022.

– Alex lets lifestyle grow with each raise.

– Sam caps lifestyle, then invests the difference.

By 2025:

– Both may have higher incomes due to inflation and raises.

– But Alex is leasing a nicer car, renting a larger place, and carrying some credit card debt. Net worth barely changed.

– Sam still drives an older car, lives in a modest place, but automatically invests a few hundred dollars every month. Even using conservative market returns from the last decade, Sam’s net worth is clearly trending up.

The key difference isn’t the job or luck. It’s that Sam used consistent financial planning to grow long term wealth, while Alex used raises to upgrade lifestyle.

—

Psychological Tricks to Stay Satisfied Without Overspending

Separate identity from spending

Lifestyle inflation often comes from trying to match an identity:

– “I’m the kind of person who drives X.”

– “People at my level don’t live in places like that.”

Instead, reframe your identity as:

– “I’m the kind of person who always lives below my means.”

– “I’m building options faster than most people I know.”

This mental shift makes “not upgrading” feel like a win, not a sacrifice.

Use “delayed yes” instead of “never”

You don’t have to say “I’ll never upgrade my car.”

Say: “If I still want this in six months and my wealth goals are on track, I’ll revisit.”

Often, six months later you either don’t care anymore – or you can afford it more comfortably.

—

When to *Intentionally* Let Lifestyle Grow

Avoiding lifestyle inflation doesn’t mean living like a student forever. It means letting lifestyle follow your wealth, not lead it.

Good times to consciously upgrade:

– Your emergency fund is full.

– You’re hitting your target savings rate (e.g., 20–30% of income).

– High‑interest debt is gone.

– You’re investing monthly without fail.

Then you can intentionally choose a few lifestyle upgrades that truly matter, instead of reacting to every raise by default.

—

Putting It All Together: A Simple Action Plan

Here’s a short, practical sequence to start this month:

– Map your current lifestyle: total monthly spending and savings rate.

– Decide a “good enough” lifestyle you can keep for the next 1–2 years.

– Set a rule for future raises (e.g., 70% to savings/investments, 30% to lifestyle).

– Automate transfers right after payday so you don’t see the “extra”.

– Once a month, check: “Did my expenses go up because of prices or choices?”

If you follow this for just a couple of years, the gap between you and your peers becomes obvious: they’ll have slightly nicer stuff; you’ll have significantly more freedom.

And that’s the real answer to how to avoid lifestyle inflation:

Treat every raise not as permission to spend more today, but as a shortcut to the life you actually want in 5, 10, or 20 years.