Why budgeting feels impossible when you’re always busy

If your days look like a sprint from alarm to bedtime, “make a detailed budget” sounds almost offensive. The issue isn’t laziness, it’s cognitive load: after work, kids, and chores, уou’ve got almost zero decision‑making energy left. That’s why classic spreadsheets fail busy people. Effective budgeting for a hectic schedule starts with accepting one fact: if your system isn’t fast, mostly automated and low‑friction, you simply won’t use it for more than a week — and that’s a design flaw of the system, not a moral flaw of yours.

Shift the goal: from control to autopilot

Instead of trying to micromanage every dollar, aim for a setup where money mostly moves without you. Think of it like setting up rails for a train: some thinking up front, then it runs on its own. Automation, pre‑decided rules and limits are your friends. The goal isn’t a “perfect” budget; it’s a “good enough” system you can manage in 10–15 minutes a week. When you evaluate any tool or tip, ask one question: “Will I realistically keep doing this when my week goes sideways?”

Inspiring case #1: The manager who stopped “budgeting”

Lena, a project manager with two kids, tried countless templates and finally gave up on budgeting. We rebuilt her process around automation. Her paycheck now lands in one account; on payday, fixed amounts auto‑transfer: rent, savings, debt, groceries, fun. She only tracks the “groceries + fun” card balance. No categories, no nightly tracking. After three months she had her first real emergency fund. Her words: “I don’t *feel* like I budget. Money just ends up in the right places.” That’s the kind of invisible system worth aiming for.

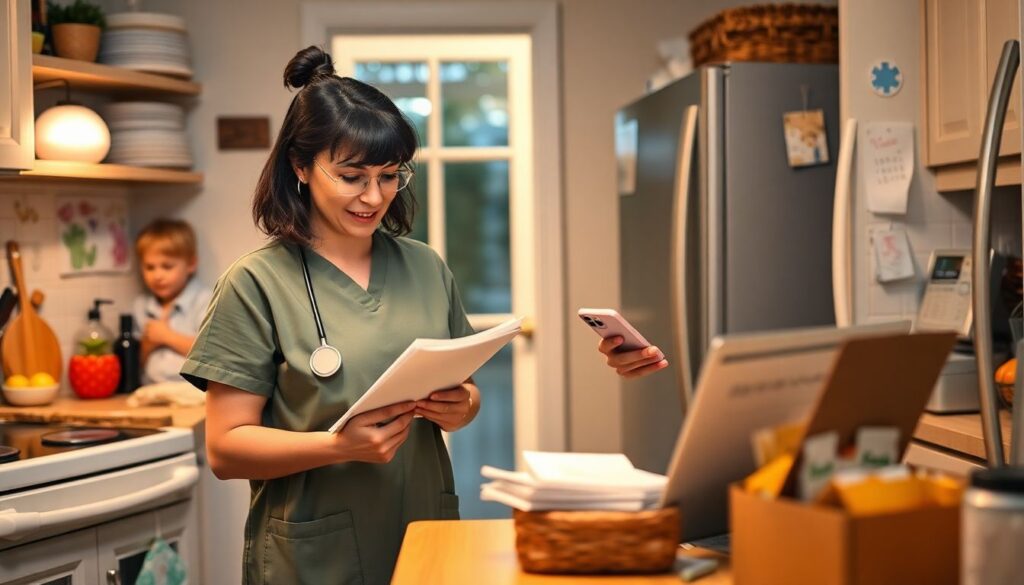

Inspiring case #2: time saving personal finance tips for working moms

Another client, Dana, a nurse and single mom, needed time saving personal finance tips for working moms, not another lecture. We focused on three rules: meal‑plan once a week, order groceries online to dodge impulse buys, and set up a “kids & surprises” sinking fund. She used one of the best budgeting apps for busy professionals but only checked one screen: upcoming bills and available cash. That tiny dashboard became her money “command center.” Result: she cut overdraft fees to zero and stopped making 11 p.m. panic runs to the store.

Tools that actually save time (not steal it)

Apps are useful only if they reduce the number of decisions you make. The best budgeting apps for busy professionals usually connect to your bank, auto‑categorize spending and show trends without you tagging every coffee. Combine them with automated savings tools for working adults that skim a small percentage from each paycheck into savings, so you grow a buffer without “feeling” the loss. For many overwhelmed workers, a simple rule like “10% auto‑saved, no questions asked” is more powerful than an elaborate, color‑coded spreadsheet.

5‑step fast‑track system for hectic schedules

1. Pick one money “command center” app and connect all accounts.

2. Create automatic transfers for rent, savings and debt on payday.

3. Use one debit or credit card for all flexible spending this month.

4. Set a simple weekly check‑in: 10 minutes on the same day each week.

5. After one month, review: which categories constantly blow up? Adjust only those.

Notice what’s missing: no daily tracking, no perfectionism, just a short routine that fits between meetings or after kids’ bedtime.

Case #3: Turning chaos into a “project”

Anton, a software lead, treated his finances like a Jira board. His problem: dozens of subscriptions, random splurges, and zero overview. We set him up with online money management services for busy people that pulled transactions into one timeline. He blocked 60 minutes on a Sunday as a “money sprint” once a month. During that sprint he killed useless subscriptions, bumped savings by 2%, and set one small “reward” purchase. After six months, he cut expenses by 18% without feeling deprived — he just managed finances like another project with a recurring review.

When to bring in a pro without wasting time

Sometimes the fastest route is getting outside eyes. Many high‑earning but overwhelmed clients decide to hire financial coach for budgeting and saving not for knowledge, but for structure and accountability. A good coach won’t drown you in spreadsheets; they’ll help you design a system that survives your ugliest weeks, then hold you to a 10–15 minute weekly ritual. Think of it as a temporary “personal trainer” for your money: intense at first, then you coast on habits. If you’re stuck replaying the same mistakes, that shortcut can pay for itself quickly.

Building skills, not just hacks

Hacks and apps are helpful, but long‑term calm comes from basic money skills: knowing your true monthly costs, planning for irregular expenses and understanding how interest works. Set a tiny education habit: 10 minutes, twice a week. Rotate between topics: debt, investing, behavioral psychology. Over a year that adds up to serious financial literacy without devouring your schedule. The point is to think more clearly, not more often, about money — clearer thinking leads to fewer emergencies and fewer late‑night “how did this happen again?” moments.

Resources you can learn from on the go

Look for resources that fit into your existing routines. Short podcasts during commutes, YouTube explainers at lunch, or mobile‑friendly blogs often beat dense textbooks. Many online money management services for busy people now bundle learning modules into their apps: bite‑sized lessons, calculators, even simulations. Prioritize creators who show numbers, timelines and trade‑offs, not just motivation. If you enjoy structure, take a short personal finance course; if not, build your own “curriculum” of three trusted voices and ignore the rest, so you don’t drown in conflicting advice.

Your money, your version of “good enough”

Budgeting for a hectic schedule isn’t about becoming the most organized person you know. It’s about designing a money system that works on your worst week, not your best. Start with one small change: maybe it’s automating savings, or a weekly 10‑minute review, or canceling three subscriptions today. Then layer on the next step once the first feels easy. Progress here is rarely dramatic; it’s quiet, almost boring. But that’s exactly the point: when money becomes boring and predictable, the rest of your life gets a lot more room to be exciting.