Most parents feel that once kids hit high school, money seems to evaporate: sports fees, phone upgrades, college prep, social life, random “I need $40 for tomorrow.” Smart budgeting for parents of teens isn’t about saying “no” to everything; it’s about building a system where you, your teen, and your long‑term goals all get a fair slice of the pie.

Below is a practical, expert‑backed guide to help you do exactly that.

—

Why budgeting changes when your kid becomes a teen

Once children move into adolescence, your household budget shifts from “basic care” to “launch preparation.” Research in the US and Europe consistently shows that spending spikes between ages 12 and 18: transportation, technology, extracurriculars, health care, and education‑related costs all climb. A 2023 youth finance survey, for instance, estimated average teen discretionary spending at over $100 a week in many developed countries, with parents quietly subsidizing a big share of that.

That means budgeting for parents of teenagers is less about diapers and daycare, and more about:

– Managing unpredictable, often social‑driven costs

– Funding big‑ticket milestones (driving, travel, test prep, college)

– Avoiding the “silent drain” of impulse, digital, and subscription spending

When you (calmly) put numbers to those categories, you stop being the “bad cop with the wallet” and become more of a coach running a family money playbook.

—

Key stats every parent of a teen should know

Over the past decade, several trends have emerged that directly affect financial planning for families with teens:

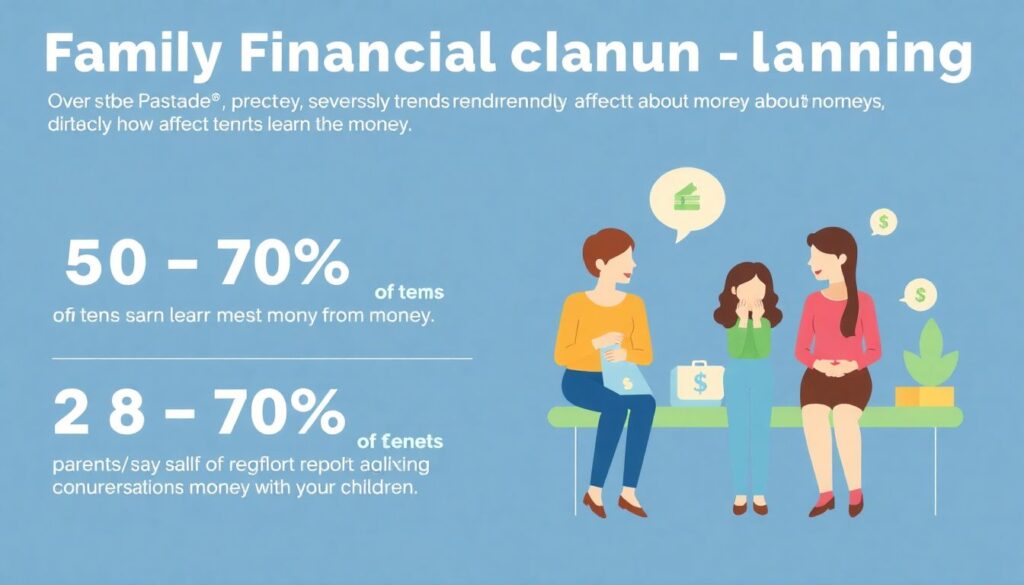

– Around 60–70% of teens say they learn most about money from their parents, but fewer than half of parents report having regular money conversations (various surveys in US, UK, EU, 2020–2023).

– Teen access to digital payments has exploded: prepaid cards, P2P apps, and in‑app purchases now account for a large portion of their spending, often invisible to parents until the bill arrives.

– College and vocational training costs have risen faster than inflation for decades, pressuring families to start saving earlier or accept higher debt later.

These numbers aren’t meant to scare you; they’re a reminder that *doing nothing* is, itself, a financial decision—with a price tag attached.

—

From chaos to plan: setting a teen‑focused family budget

A good family budget planner for parents of teens doesn’t just slice expenses by category; it lines up today’s spending with tomorrow’s launches: driving, graduation, college, moving out, or gap year. Financial planners often suggest three “buckets” as a starting point:

– Now costs – recurring items: food, transport, phone, sports, clubs, pocket money

– Soon costs – 6–24 months away: trips, big tech upgrades, test prep, sports camps

– Later costs – 2+ years away: car purchase help, college fund, emergency buffer

Once these buckets are clear, you can sit down with your teen and say something like:

“Here’s what we can realistically do this year. If we put more into ‘later,’ it will mean less ‘now.’ Let’s decide together what actually matters.”

That conversation alone is a powerful piece of financial education.

—

Expert strategies for aligning teen spending with family values

Financial therapists and CFPs (Certified Financial Planners) who work with families of adolescents keep repeating one insight: *teens are far more reasonable when they see the full picture.* Hidden budgets breed conflict; shared frameworks create buy‑in.

Experts typically recommend you:

– Name your top 3 family money priorities (for example: college, debt‑free living, travel).

– Set clear “who pays for what” rules: which costs are on you, which on your teen, and which are shared.

– Use written agreements for gray areas—such as driving costs or streaming services—so the rules don’t change mid‑argument.

When everyone knows the rules before the temptation appears—new phone, brand‑name shoes, last‑minute concert—decisions become less emotional and more consistent.

—

Practical steps: building a teen‑inclusive budget in 30 days

You don’t need a full financial overhaul to start. Give yourself a month and follow a simple weekly plan:

– Week 1 – Track everything

You and your teen both record every expense for seven days. No judging, just data. At the end of the week, circle “surprise” categories—things you didn’t realize cost so much (often food delivery, gaming, transportation).

– Week 2 – Set guardrails, not handcuffs

Create spending ranges for key teen‑related categories: eating out, clothing, activities. Guardrails mean: “We aim for $X–$Y per month; if we hit the upper limit early, we pause.”

– Week 3 – Introduce shared tools

Choose 1–2 tools you’ll actually use together: maybe a shared calendar for big upcoming costs and one app for tracking allowances and teen spending.

– Week 4 – Review and renegotiate

Sit down for 30 minutes. What worked? What felt tight? Adjust by small increments, not huge swings. This cements the habit instead of triggering rebellion.

By the end of these four weeks, you’ll have a living system rather than a theoretical budget hiding in a spreadsheet.

—

Tech to the rescue: choosing the right apps

The best budgeting apps for families with teenagers have three traits: transparency, simplicity, and teen‑friendly interfaces. You want tools that let you see where money goes without micromanaging every soda or bus ride.

Look for features like:

– Separate teen accounts or “jars” with spending limits

– Real‑time alerts on purchases, so you can talk about issues while they’re small

– Goal‑tracking for specific teen targets (laptop, trip, first car)

– Options to tie chores or tasks to pocket money or “earnable” categories

Many experts warn against over‑surveillance; teens need some privacy and room to make low‑risk mistakes. Choose tech that supports conversation, not control.

—

How to teach teens about money and budgeting without lectures

Most teens tune out when they hear phrases like “compound interest” or “cash flow.” To keep it real, link money lessons to things they already care about: freedom, identity, and social life.

You can weave learning into daily life like this:

– When they want a big purchase, walk them through comparing prices, reading reviews, and calculating how many work hours or chore weeks it equals.

– Before school trips or vacations, give them a fixed budget and let them decide how to spend it—then debrief after.

– When subscription renewals pop up, show them how tiny monthly amounts stack into large yearly costs.

This is the heart of how to teach teens about money and budgeting: repeated, small, real‑world decisions, followed by short, non‑judgmental conversations about what went right and what didn’t.

—

Economic realities: why planning ahead matters more now

From a broader economic angle, parents of teens today are squeezed from multiple directions. Housing, healthcare, and education costs have grown faster than wages in many countries. At the same time, the job market your teen will enter is more volatile, with automation and AI reshaping entry‑level work.

For you, that means every unplanned $100–$200 teen expense is competing directly with retirement savings, emergency funds, or debt repayment. Financial planning for families with teens is really about creating resilience: can your household absorb shocks—a car repair, a medical bill, a sudden school fee—*and* still support your teen’s progress?

Families who intentionally carve out even modest sums for “future teen costs” tend to rely less on high‑interest credit card debt later. That’s a quiet but crucial win.

—

What experts predict: teens, money, and the near future

Looking ahead 5–10 years, economists and education researchers see several trends that will shape how your teen handles money:

– More cashless spending – Physical cash will keep shrinking; your teen will live in a tap‑and‑scan world, which often feels “less real” and therefore more easily overspent.

– Earlier income streams – Side hustles, gig work, online freelancing: teens are already earning in new ways, but often without guidance on taxes, saving, or boundaries.

– Greater pressure to “keep up” – Social media intensifies comparison: clothes, travel, tech, lifestyle. That emotional pressure often shows up as financial pressure on parents.

Experts expect that families who actively teach digital money skills—verifying sources, avoiding scams, reading terms, understanding recurring vs one‑time charges—will give their teens a tangible advantage in this environment.

—

Impact on the financial and education industries

The way parents are handling teen money today is reshaping entire sectors. Banks, fintech startups, and educational platforms have realized that if they build loyalty in the teen years, they may gain customers for life. That’s why you’re seeing:

– Debit cards and accounts specifically marketed to teens, with built‑in parental controls

– Apps that blend gamified saving, short financial literacy lessons, and real money management

– High schools partnering with financial institutions or nonprofits to deliver personal finance modules

Your choices—where your teen banks, what tools you trust, which platforms you ignore—signal demand. When large numbers of parents prioritize transparency, low fees, and strong educational content, companies adapt their products. In other words, how you handle budgeting at home nudges the entire industry’s direction.

—

Common money traps for parents of teens (and how to dodge them)

Even well‑intentioned parents often fall into a few predictable patterns that undermine their goals:

– The “ATM parent” habit – Handing over cash or instant transfers with no follow‑up, then wondering why money “disappears.”

– Rescuing from every mistake – Covering overdrafts, replacing lost phones, or quietly paying off in‑app purchase binges without involving your teen.

– Inconsistent rules – Saying “we can’t afford this” one week and blowing the budget the next, which teaches teens that money limits are negotiable stories, not real constraints.

The antidote is simple, but not always easy: clear agreements, consistent follow‑through, and calm, scheduled check‑ins instead of crisis‑driven arguments.

—

Designing your own “family money system” with teens

Think of your household as running a small, values‑driven business. You have income, expenses, assets, and goals. Your teen is not just a cost center; they’re a trainee partner in running that operation.

To build your system, pick a few guiding rules:

– Every month, you and your teen review upcoming costs for the next 60 days.

– Any request over a certain amount (say, $50 or $100) waits 24 hours before you decide.

– A percentage of all teen income (allowance, gifts, job earnings) is split between saving, giving, and spending.

Over time, this turns random money fights into predictable, calmer routines.

—

Bringing it all together

Smart budgeting for parents of teens isn’t about perfection or spreadsheets worthy of an accountant. It’s about designing money habits that can survive real life: busy weeks, changing moods, sudden opportunities, and the occasional teenage meltdown.

If you remember only three things, let them be these:

– Make the budget visible and shared, not secret.

– Use tech as a bridge to conversation, not as a surveillance tool.

– Treat every money decision as a tiny training session for your teen’s future independence.

Do that consistently, and the “budget talk” stops being a battlefield and becomes one of the most useful gifts you can give your almost‑adult child.