Why money feels different when you’re an immigrant student

Money stress hits immigrant students harder because you’re often juggling two worlds: your life in the new country and expectations back home. In 2025 tuition keeps rising faster than inflation in the US and UK, and part-time jobs rarely keep up. Your parents may still think in terms of what university cost 20 years ago, while you’re looking at $30,000–$60,000 a year for tuition alone. Add rent, health insurance, visas, flights, and suddenly every coffee feels like a financial decision. That’s why you need personal finance systems that respect both your academic goals and your immigrant reality, not just generic “don’t buy lattes” advice.

From foreign students to global consumers: a quick history

A bit of context helps. In the 1970s–1980s, most international students either came on full scholarships or had wealthy families; banks didn’t care about them as retail clients. By the 2000s, education turned into a global business: countries like the USA, Canada, the UK and Australia started seeing students as both talent and customers. After the 2008 crisis, governments tightened work rules, but universities raised fees. Fast‑forward to 2025: fintechs chase students with apps and cards, while visa rules and housing costs keep getting tougher. Knowing this history explains why you’re flooded with offers, yet still struggle to open a simple account or build credit.

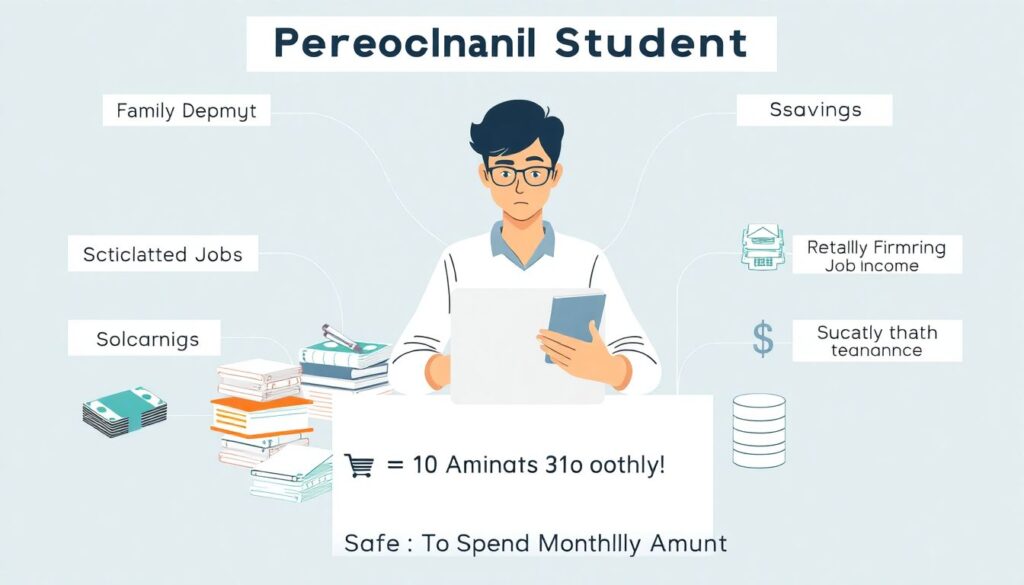

Step one: turn your situation into numbers, not vibes

Before looking for personal finance tips for international students, you need a brutally honest snapshot of where you stand. List *all* guaranteed money for the academic year: family support, scholarships, savings, and realistic job income. Divide that by 10 months to get your “safe to spend” monthly number. Then list non‑negotiables: tuition, fees, rent, health insurance, minimum phone and transport. Whatever is left is your real lifestyle budget, not the number in your bank app. Many immigrant students never do this calculation and end up overspending in the first semester, then scrambling with extra shifts right before exams.

Practical budgeting: a simple system that survives midterms

When people ask how to budget as an international student in the USA or elsewhere, the mistake is overcomplicating things with 20 categories you’ll stop tracking in week two. Use a 3‑bucket method: “must pay”, “study & future”, “flexible fun”. A common split is 60/20/20, but if your rent is brutal, 70/20/10 may be more realistic. Automate transfers on payday: as soon as money hits, move next month’s rent and basic bills to a separate “boring” account so you can’t accidentally spend it. Whatever remains in your main account is your actual room for food, transport, and modest fun without guilt.

Real‑life example: Aya’s first semester mistake

Aya arrived from Morocco to a US state university with $10,000 from her parents, thinking it would last two semesters for living costs because prices “didn’t look that bad.” She didn’t account for mandatory health insurance ($2,400 a year), lab fees, and deposits for housing and utilities. By November, she had burned through $7,000 and started skipping meals to avoid asking her family for more. When we turned her situation into a budget, her sustainable monthly spend was actually $850, not the $1,300 she had been using. The fix wasn’t magical: she renegotiated her meal plan, took a library job, and moved to a shared room.

Technical block: quick monthly budget formula

– Annual guaranteed money = family support + scholarships + savings drawdown + realistic part‑time income

– Subtract *all* fixed annual costs: tuition, mandatory fees, insurance, visas, flights, housing deposits amortized over the year

– Result ÷ 10 = safe monthly spending limit (not including summer)

– Aim:

– 60–70% necessities (rent, food, phone, transport)

– 10–20% study and future (books, software, exam fees, small savings)

– 10–20% flexible fun (social life, travel, eating out)

Recalculate every semester when any of the inputs change.

Banking basics: make the system work for you

Opening your first account abroad can feel like solving a puzzle with missing pieces: no Social Security number, no local credit history, maybe no utility bill in your name. Still, choosing the best bank accounts for international students is worth the effort because fees quietly eat your budget. Prefer accounts with: no monthly maintenance fee, free or cheap international transfers, and a large ATM network near campus. In 2025, many online‑only banks and credit unions accept passports plus I‑20 or enrolment letters. Ask international student services which banks have a history of approving people from your country.

Technical block: what to check when opening an account

– Monthly fee and minimum balance requirement

– ATM withdrawal fees on and off campus

– Foreign transaction fees (often 0–3%)

– Incoming international wire fee (can be $0–$20)

– Overdraft policy: do they decline or allow negative with big fees?

– Mobile app functions: freeze card, instant alerts, budgeting tools

– Ability to add a parent abroad as sender or joint user

Take photos or screenshots of all fee pages; when you’re tired and busy, those fine‑print details are easy to forget.

Building credit from zero: do it early and carefully

Access to credit is often where immigrant students get stuck or trapped. Back home, you might rely on cash and family; in the US or UK, your credit score affects housing, phone plans, sometimes even jobs. Fortunately, there are now student credit cards for international students with no credit history, especially secured cards where you deposit, say, $300 as collateral and get a $300 limit. Use it only for one recurring expense, like your phone bill, and set automatic full payment each month. After 6–12 months, you may qualify for an unsecured card and start building a real credit profile.

Spending cuts that don’t wreck your social life

The question isn’t just how to save money as an international student abroad; it’s how to do it without isolating yourself. Start with the big levers, not tiny sacrifices. Housing: sharing a room or living one bus stop farther can save $200–$400 a month. Food: cooking 70% of your meals can easily cut your costs in half compared to eating on campus daily. Transport: a student public transit pass is usually cheaper than owning a car, especially once you add insurance and parking. Keep some money earmarked for low‑cost social activities—picnics, potlucks, campus events—so you don’t feel punished by your budget.

Smart earning: work that fits your study rhythm

Many immigrant students underestimate how draining part‑time work can be during exam season. A better question than “how many hours can I legally work?” is “how many hours can I work without sabotaging my GPA and health?” On US F‑1 visas, you’re capped at 20 hours per week on‑campus; realistically, 10–15 is sustainable for demanding majors. Prioritize jobs that align with your schedule and long‑term goals: library, tutoring, research assistant, lab monitor. They may pay slightly less than restaurant or delivery work, but the lower stress and networking opportunities often pay off more over a few years.

Technical block: evaluating a part‑time job

Ask yourself:

– Hourly pay after taxes vs. commute time and prep (uniforms, transport)

– Predictability of schedule during midterms and finals

– Impact on sleep: will you regularly be home after midnight?

– Skill value: does this build language, tech, or people skills useful later?

– Legal status: strictly within your visa rules?

Run the math: extra $150 a month is not worth a chronic sleep debt that drags your grades and future salary down.

Mindset shifts: from “surviving” to planning ahead

Growing up in economic uncertainty, many immigrant families focus on survival: pay this semester’s tuition, worry about the rest later. That mindset helps in crisis but hurts long‑term planning. Start acting like your own small financial manager. Set three horizons: this month (cash flow and bills), this year (tuition, visas, travel), and 3–5 years (graduation, work visa, maybe moving cities). Even saving $30–$50 a month into a separate “future” account builds the habit. It also creates a tiny emergency fund so one broken phone or surprise fee doesn’t force you into high‑interest debt or awkward calls home.

Using tech without letting it use you

Budgeting apps, multi‑currency wallets, and fintech cards boomed after 2020, and many are specifically marketed toward young migrants. They can be lifesavers—for example, apps that show real‑time exchange rates and low‑fee transfers to your home country. But be cautious with features that encourage overspending, like instant “buy now, pay later” for clothes or gadgets. Pick one main app for tracking expenses, connect only the accounts you actually use, and review your spending once a week. If a tool makes you feel constantly guilty or stressed, switch. The best system is the one you’ll still be using in exam week.

When family expectations collide with financial reality

A quiet pressure for many immigrant students is sending money home or maintaining an image of success. Your relatives may assume that “abroad” equals “rich,” not realizing your rent alone could be half a typical monthly salary back home. Be transparent—with numbers, not drama. Share your actual budget in your home currency: tuition, rent, income limits. Explain visa work restrictions and the real cost of flights. You don’t need to overshare every struggle, but honest context reduces guilt on both sides and helps your family support smarter decisions instead of pushing you toward risky side hustles.

Putting it all together without burning out

Balancing budgets and studies as an immigrant student is less about perfection and more about setting guardrails. You need a simple budget that survives busy weeks, low‑fee accounts that don’t quietly drain you, early and cautious credit building, and work that supports rather than sabotages your degree. Pick one thing to implement this week: maybe open a no‑fee student account, set up a basic 3‑bucket budget, or apply for a secured card. You are not just “getting through school abroad”; you’re building the financial habits that will shape your entire life after graduation.