Rethinking what “tax saving” really means

Most people google best tax saving investment options and then blindly buy whatever their friend or banker suggests in March. That’s not tax planning, that’s panic shopping. Smart saving starts earlier: you decide which income you want to protect, for how long you’re ready to lock money, and what risk you can survive without losing sleep. Then you choose tools that fit this plan instead of chasing random deductions. When you think this way, every new dollar has a “job”: either lower current tax, shift tax to the future on better terms, or turn fully taxable income into something taxed at a lighter rate or not taxed at all.

Real case: turning bonuses into low‑tax wealth

Imagine Anna, 32, getting big but irregular bonuses. At first she kept them in a savings account and paid full income tax every year. Her advisor helped her build investment plans to save income tax in a layered way: part of each bonus went into a retirement account with deductions now, another slice into long‑term equity funds with favorable capital‑gains treatment, and a small portion into municipal‑style bonds with tax‑friendly interest. Over five years she didn’t earn less; she just rearranged the “buckets.” Net result: same gross income, but her effective tax rate on bonuses dropped several percentage points, and the compounding on the tax she didn’t pay started working for her instead of the government.

Real case: freelancer stabilizing messy taxes

Now take Mark, a freelance designer with income jumping all over the place. Some years he was pushed into a high bracket, other years were weak. Instead of guessing, he used flexible investment plans to smooth his tax hits. In strong months he overfunded tax‑advantaged accounts, then complemented them with tax efficient investment strategies in a normal brokerage: realizing losses to offset gains, preferring long‑term holdings, and favoring tax‑light index funds. He even set up a small retirement plan for his business to shelter a chunk of profit. The trick wasn’t magic products; it was using boring tools in a deliberate order tied to his uneven cash flow.

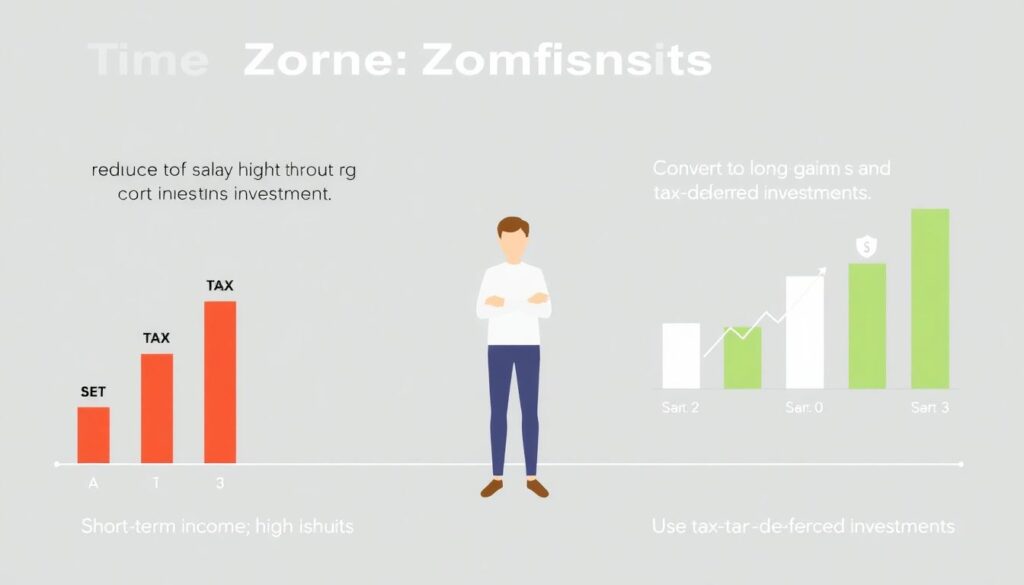

Non‑obvious move: tax planning by “time zoning”

When people ask how to reduce taxes through investments, they usually think only about this year. A smarter, less obvious angle is “time zoning” your tax burden. Short‑term income from salary and side hustles tends to be taxed highest, so you aim to convert part of it into long‑term gains or tax‑deferred income that lands in years when your bracket will likely be lower (career break, early retirement, relocation). That can mean prioritizing growth assets you intend to hold for years, using retirement accounts not only for old age but as a tool to shift tax to a future, cheaper you, and avoiding frequent trading that constantly resets the tax clock.

Non‑obvious move: using debt and location cleverly

Another under‑used tactic is combining investments with debt and geography. Instead of paying down a very cheap mortgage aggressively, some investors keep it and direct surplus cash into vehicles with better after‑tax returns, effectively letting low‑cost debt finance higher‑yield, tax‑favored assets. Others plan future relocations to lower‑tax regions and line up assets whose taxation is triggered only when they sell. By holding until after the move, they legally face gentler rules. None of this is about evasion; it’s about synchronizing where and when gains become taxable with the moments in your life when the tax bite will be smallest.

Alternative methods beyond the usual funds

Everyone knows about top tax saving mutual funds and plans, but they’re not the only game in town. Depending on your country’s rules, you may tap instruments like tax‑advantaged municipal‑style bonds, government‑incentivized retirement schemes for the self‑employed, or even structured notes that repackage returns into more tax‑friendly forms. Some people ignore company stock plans or employee purchase programs that offer discounts and deferred taxation, leaving free money on the table. Others can use life‑insurance‑based wrappers not for protection only, but as long‑term tax shelters for investments they’d hold anyway. The key is not to buy complexity for its own sake, but to pick alternatives where the tax edge clearly outweighs the extra costs and restrictions.

Alternative angle: investing in skills and timing income

A quietly powerful alternative method isn’t about products at all; it’s about your earning pattern. If you’re on the verge of a higher tax bracket, it may be smarter to invest in a short course or certification that pushes your long‑term income up, while deferring some current earnings or bonuses into next year using employer plans. Paired with the right investment vehicles, this can compress taxable income into more efficient bands over several years. It’s less glamorous than hunting the best tax saving investment options, but in practice, strategically shaping when and how you earn — then routing that cash through tax‑aware investments — often beats chasing small percentage advantages on a single fund.

Five smart, less‑obvious tactics you can copy

1. Treat losses as assets, not failures. Realized investment losses can offset gains and, in some systems, even salary. Deliberately harvesting modest losses from lagging positions, while keeping your overall allocation intact, turns market noise into tax savings. Done carefully, this is one of the most practical tax efficient investment strategies available to ordinary investors.

2. Split strategies by account type. Put high‑yield, heavily taxed assets into tax‑sheltered accounts, and keep low‑turnover, tax‑light holdings in taxable ones. Many investors reverse this and quietly leak money in unnecessary taxes every year.

3. Automate “March madness” prevention. Set recurring investments into tax‑favored vehicles throughout the year so you’re not forced into bad last‑minute choices.

4. Use family bandwidth. Where rules allow, shifting contributions between spouses or funding accounts for children can expand your overall tax‑favored envelope.

5. Always compare net, not gross. A flashy return that’s taxed harshly may leave you with less in hand than a quieter, tax‑gentle alternative.

Pro‑level lifehacks for seasoned investors

Once the basics are in place, professionals go deeper. They simulate their future tax brackets, model different retirement ages, and then design layered investment plans to save income tax over decades, not just a single year. They keep a running “harvest list” of positions ideal for realizing gains or losses in specific tax years. They also coordinate employer stock, options, and bonuses, staggering exercises and sales so they don’t all pile into the same expensive bracket. Instead of asking only how to reduce taxes through investments today, they keep asking, “If I trigger this gain now versus in three years, what is the after‑tax difference?” That simple habit often adds more value than chasing the next hot product.