Why International ETFs Deserve a Spot in Your Portfolio

If your investment apps and news feeds talk mostly about U.S. stocks, you’re seeing only half the market. Roughly 40–45% of global stock market value is outside the U.S., and that slice includes mature giants in Europe, fast‑growing Asian tech names, and often cheaper valuations than on Wall Street. International ETFs let you own all of that with a couple of clicks, without opening foreign brokerage accounts or worrying about currency conversions on every trade. For a beginner, they’re usually the simplest way to turn a “home‑biased” portfolio into a genuinely global one, spreading risk across economies, regulations and currencies instead of betting your entire future on one country.

What Exactly Is an International ETF?

An international ETF is a basket of foreign stocks (or bonds) you buy as a single share on your local exchange. For example, one share of a broad fund might hold exposure to thousands of companies from Europe, Japan, Australia, emerging markets like India and Brazil, and everything in between. The fund manager handles all the complexity: foreign exchanges, dividend taxes, currency conversions. You just see a price in your home currency and a ticker symbol. For beginners, this is typically the best international etf for beginners approach: cheap, broad, rules‑based index funds instead of hand‑picked foreign stocks you can’t easily research or even trade during your waking hours.

> Technical note: how an ETF actually gives you foreign exposure

> Most international ETFs are “physical” — they actually own the foreign stocks in local markets and hold them via custodians. A few use derivatives (swaps, futures), especially in niche markets, which adds counterparty risk. Check the fund’s factsheet for “replication method”: “physical” or “sampling” is generally simpler and more transparent for a beginner than synthetic structures.

Why Bother Going Global If the U.S. Has Been Winning?

Over the last 15 years, U.S. equities crushed many foreign markets. From 2009 to 2024, the S&P 500 delivered roughly 11–12% annually, while broad international developed markets hovered closer to 5–7% per year depending on the exact index. But that leadership is cyclical. In the 1970s and 1980s, international stocks outperformed the U.S. for long stretches. Japan was the superstar in the late ’80s, and emerging markets had huge runs in the 2000s. Nobody rings a bell when leadership changes. Adding international exposure is less about guessing the next winner and more about building a portfolio that survives different regimes: strong dollar, weak dollar, high inflation, slow growth, energy crises, and political shocks that may hit one region much harder than others.

A Simple Framework: Core, Satellite, and Your Home Bias

Think of your portfolio as a planet: the core is your main global equity holding, and satellites are more focused bets. An effective international etf investment strategy for beginners usually starts with a global core, then dials in extra exposure where it makes sense. One common structure is 60–70% domestic stocks and 30–40% international within the equity bucket. If your job, salary, house and pension are all tied to one country, adding a meaningful foreign slice reduces the “everything depends on my country” risk. You don’t need to micromanage each region: one or two broad international ETFs can quietly rebalance the world for you inside a single ticker, while you focus on earning and saving instead of guessing which country will outperform next year.

> Technical note: deciding your international allocation

> • Classic 60/40 portfolio: many planners suggest 20–40% of your stock allocation in international.

> • Market‑cap weight: global equity is ~55–60% U.S., ~40–45% ex‑U.S. Owning that proportion is the “neutral” stance.

> • Risk trade‑off: more international means more currency volatility and sometimes more political risk, but usually lower dependence on a single market’s valuation level.

How to Invest in International ETFs Step by Step

If you’re wondering how to invest in international etfs without turning it into a second job, use a checklist approach. First, check what your broker offers commission‑free, because trading fees eat into small contributions. Second, decide if you want “all countries outside my home” or to exclude your own market explicitly. For a U.S. investor, a “total international” ETF covers both developed and emerging markets in one shot, while a European or Asian investor might mix a global ex‑local ETF with a separate domestic fund. Third, set an automatic monthly contribution so you buy through booms and busts, instead of trying to time currency or political news. The process should feel boring after a few months; that boredom is a feature, not a bug.

Real‑World Example: A Beginner in the U.S. Adding International

Imagine Alex, 28, based in Texas, who has only a U.S. total market ETF in a Roth IRA. They earn $70,000 a year and can save $500 monthly. Alex decides to shift toward a global portfolio over a year. Instead of dumping everything at once, Alex allocates the next 12 monthly contributions as 70% U.S. total market and 30% international ETF. After a year, roughly 15–20% of Alex’s equities are international. Five years later, the U.S. market has a flat stretch while international stocks, especially in India and parts of Europe, do better. The portfolio doesn’t skyrocket, but that foreign slice smooths returns: Alex sees smaller drawdowns and better diversification. No heroic trades, just a pre‑planned ratio and automatic purchases.

What “Low Cost” Really Means in International ETFs

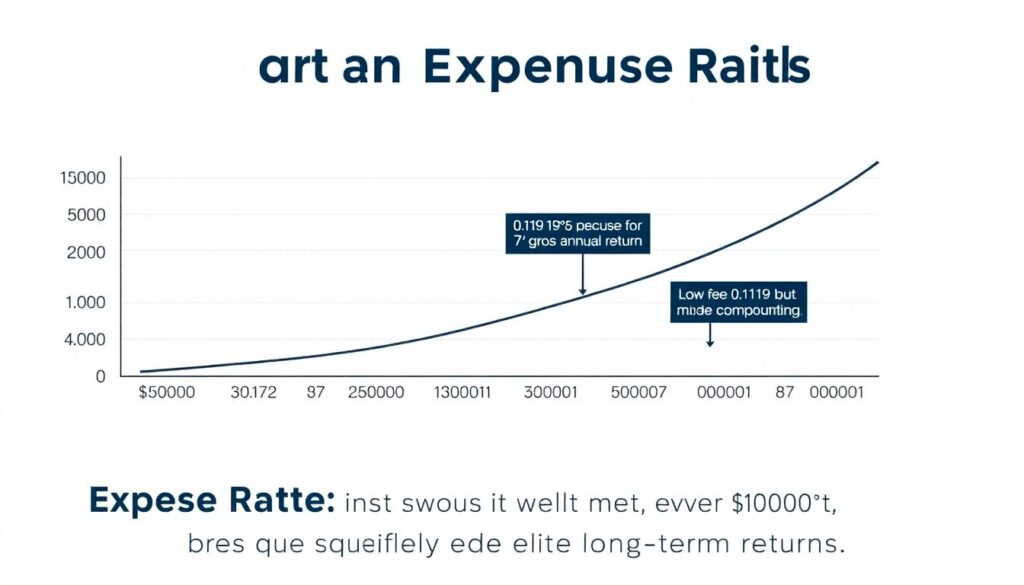

When you’re comparing funds, expense ratio looks tiny in isolation — 0.11% vs 0.19% sounds trivial. Over decades, it’s not. On a $50,000 investment held for 30 years at 7% gross return, the difference between 0.10% and 0.40% annual fees can exceed $10,000 in missed compounding. That’s why the top low cost international index funds and etfs get so much attention from long‑term investors. Cost is one of the few variables you control completely: you can’t predict currencies or economic cycles, but you can certainly avoid paying an extra 0.5% every year for a fund that tracks the same index. For a beginner, an international ETF with total fees below 0.20–0.25% is usually a solid benchmark; much higher and you should demand a very good reason.

> Technical note: the hidden costs beyond the expense ratio

> • Bid–ask spread: a wide spread means you pay more to get in and out. For liquid international ETFs, spreads can be a few cents; for niche markets, much more.

> • Tracking difference: some funds lag their index by more than the stated expense ratio due to tax drag, trading costs and securities lending policies.

> • Withholding tax: foreign governments may tax dividends before they reach you; structure and domicile of the ETF influence whether you can reclaim part of it.

Vanguard, iShares and Others: You Don’t Need 10 Funds

Big providers compete on cost and scale, which is great for you. A typical vanguard international etf comparison versus, say, an iShares equivalent often shows nearly identical holdings, very similar returns, but slightly different expense ratios and volumes. One fund might charge 0.07%, the other 0.09%, while tracking almost the same MSCI or FTSE index. In that case, you can safely prioritize low cost and liquidity instead of stressing over microscopic differences in country weights. The danger for beginners is not picking the “wrong” international ETF; it’s scattering money across too many overlapping funds, then losing track of what you actually own. One or two broad funds usually beat a messy pile of regional ETFs with tiny positions.

Unconventional Angle #1: Use Currency to Your Advantage Instead of Fearing It

Many new investors worry that currency moves will ruin their returns. In reality, currency risk can act as a shock absorber. For example, if your home currency weakens while foreign markets are flat, your international ETF in local‑currency terms can still rise because each euro or yen is now worth more at home. An unusual but practical approach is to deliberately own international ETFs in markets where your future spending might occur — for instance, if you dream of retiring part‑time in Portugal, holding some euro‑denominated exposure today helps hedge that future lifestyle cost. Instead of treating currency volatility as an enemy, you can frame it as a long‑term hedge against the uncertainty of where you’ll actually live, work and spend in 20–30 years.

Unconventional Angle #2: Pair International Stocks with Local “Career Risk”

Most people think of diversification in terms of asset classes, not careers. But your job is effectively a giant undiversified asset tied to your local economy. If you work in U.S. tech, a slowdown in that sector might hurt both your income and the value of your domestic tech stocks. One creative international etf investment strategy for beginners is to map your career risk loosely to regions and sectors, then lean your investments the other way. A software engineer heavily exposed to Silicon Valley might intentionally overweight international value and dividend‑heavy markets like Europe or parts of Asia, so that they are not doubling down on the same growth story that pays their salary. The goal isn’t perfect hedging; it’s simply to avoid being “all‑in” on one narrative.

How to Pick Among Broad International Options

Choosing the best international etf for beginners usually comes down to four questions: How broad is the coverage? Are emerging markets included? How low are the fees? How easy is it to trade? For instance, some funds track “developed markets ex‑U.S.” — mostly Europe, Japan, Canada, Australia — while others cover “all‑country ex‑U.S.,” which adds emerging economies like India, Brazil, and South Africa. If you prefer a single‑ticket solution, the latter can be more convenient. Then check fund size (larger funds tend to be more liquid) and average trading volume. Finally, confirm that your broker offers it at low or zero commission. If two funds are nearly identical, don’t overthink it; pick the one you’re comfortable holding for 20 years, because switching back and forth invites emotional trading.

> Technical note: developed vs emerging markets in indices

> • Developed markets: typically include Western Europe, Japan, Canada, Australia, Hong Kong, Singapore. Usually more stable, slower growth, lower volatility.

> • Emerging markets: include China, India, Brazil, South Africa, Mexico, Indonesia and others. Often faster growth, but higher political and currency risk.

> • Weighting: in many “total international” indexes, developed markets might account for ~75–80% and emerging ~20–25%.

Real‑World Example: A European Investor Avoiding Home Overload

Take Lena, 35, living in Germany, already has plenty of euro exposure: salary, pension, property. She originally bought a Europe‑only ETF because it felt familiar. Over time, her portfolio became 90% European stocks, with almost no exposure to the U.S. or Asia. After revisiting her plan, Lena decides to gradually sell part of the Europe fund and buy a global ex‑Europe ETF that focuses on North America and Asia‑Pacific. Over five years, her portfolio shifts to about one‑third Europe, two‑thirds rest of world. That mix cushions the impact when European markets enter a shallow recession while U.S. and Indian stocks keep growing. Instead of trying to time economic data, Lena used geography as a risk control tool.

When Niche International ETFs Make Sense (and When They Don’t)

You’ll see glossy ads for “frontier markets,” “China tech” or “Asia consumer” ETFs. They sound exciting, and sometimes they do produce eye‑catching returns — but usually with stomach‑churning drops in between. For a beginner, these should be satellites, not the core. After you’ve built a solid base of broad exposure, you might allocate a small slice, maybe 5–10% of your equity, to a theme you understand and are willing to hold through large drawdowns. The test is simple: if this niche fund went down 50% and stayed there for three years, would you panic and sell? If the honest answer is yes, you’re better off strengthening your core and ignoring the fancier tickers crowding your watchlist.

Using Comparisons Wisely: Don’t Chase Last Year’s Winner

It’s tempting to open a vanguard international etf comparison chart, see which fund did best over the last 12 months, and buy it. That’s essentially a performance‑chasing strategy, and it often backfires because leadership rotates. A more grounded approach is to compare funds on three dimensions you control: fees, diversification and simplicity. If two international ETFs track very similar indexes, the slightly cheaper one with broader holdings and strong liquidity is usually the rational choice, even if its recent performance looks a bit worse. The market doesn’t care when you started watching the chart; it only cares what you’re holding now. Your future returns depend much more on staying invested through cycles than on shaving a few basis points by guessing the next hot region.

Putting It All Together: A Practical Roadmap

To wrap this into a concrete plan, outline your steps: decide your target international percentage within your equity allocation; select one or two broad, low‑cost international ETFs that include both developed and emerging markets; set a monthly investment amount; and review once a year, not every week. On that annual date, rebalance back to your targets if one region has run far ahead. If you feel an itch to tinker in the meantime, channel it into reading fund factsheets, understanding tax rules, or refining your long‑term goals instead of compulsive trading. Over time, the habit of steady contributions and rare, deliberate adjustments will likely matter more than any clever tweak to your choice of fund.

By starting with a simple structure and adding nuance only when you genuinely understand it, you turn “international investing” from something intimidating and exotic into just another calm, rules‑based part of your financial life.