Why Downsizing in 2025 Is About Freedom, Not Loss

Moving to a smaller place used to feel like defeat: in the 1950s the “dream” was a big suburban house, a garage and a lawn to mow every weekend. But after the 2008 crisis and особенно после пандемии, people started questioning that script. In 2025 budgeting for downsizing to a smaller home is more about buying back time, flexibility and options. Money you don’t pour into extra rooms, utility bills and endless repairs can support travel, retraining, or just a calmer life. The key is to treat your move as a strategic project, not a rushed escape.

A Quick Historical Detour: How We Got Hooked on Big Houses

In the 20th century, especially after World War II, governments promoted homeownership as a symbol of stability. Cheap mortgages and highway construction pushed families to bigger and bigger homes. By the 1990s in the US, average new homes were almost twice the size of those in the 1950s. Then came housing bubbles, climate concerns and remote work. The cost of moving to a smaller house and saving money suddenly started to look rational, not radical. Today, with rising interest rates and energy prices, downsizing fits into a broader shift: less stuff, more resilience, smarter budgeting.

Step Zero: Mindset Before Numbers

Before you open a spreadsheet, notice what you feel when you imagine a smaller home. Many people bump into status anxiety: “What will others think?” History shows how fragile that is — just think of all the “forever homes” sold after each recession. In reality, the people who handle how to plan a moving budget for downsizing early often bounce back faster from economic shocks. Treat every square meter as a line item: if a room is rarely used, it’s silently charging you via heating, cleaning, taxes and mental load. Your budget simply makes that visible.

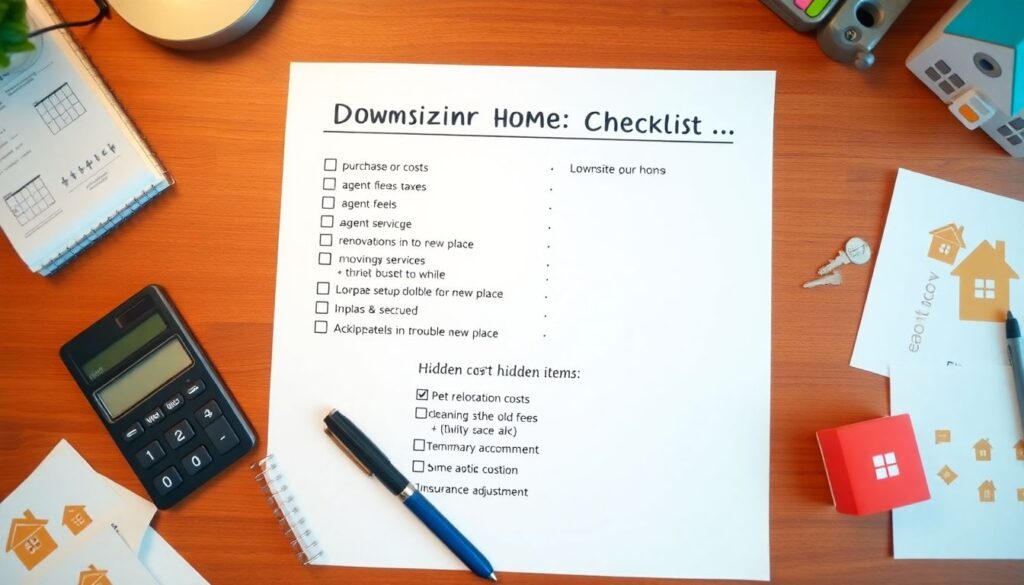

Core Budget Blocks: What to Count and When

A realistic financial checklist for downsizing your home starts months before you pack the first box. Add purchase or rent costs, taxes, agent fees, moving services, storage, renovations in the new place, and overlap costs if you pay double housing for a while. Then include hidden items: pet relocation, parking permits, internet installation, furniture that won’t fit, temporary childcare or time off work. Bring in 10–15% as a buffer: history of big moves — from postwar resettlements to recent urban migrations — показывает, что люди почти всегда недооценивают мелкие траты и срочные покупки.

1. How to Plan a Moving Budget for Downsizing, Step by Step

1. Define your “why”: lower stress, early retirement, new city, health.

2. Map your current costs: mortgage or rent, insurance, utilities, commuting, maintenance.

3. Model your future costs realistically, using prices for 2025 in your region.

4. Compare three scenarios: optimistic, base and conservative.

5. Decide hard limits: maximum moving budget and acceptable temporary debt.

6. Track actual expenses weekly once the process starts.

This turns an emotional leap into a controlled experiment, where every spending choice gets tied back to your main goal.

Inspiring Real-Life Examples

Take a couple in their mid‑40s who swapped a 4‑bedroom suburban home for a compact city apartment. Their friends thought they were “going backwards”, yet within two years they had cleared all credit card debt and built a decent emergency fund. Because they had done careful budgeting for downsizing to a smaller home, they cut commuting, heating and property tax costs. They used the freed‑up cash to pay for a career change and part‑time study. Emotionally, the biggest surprise was not feeling cramped, but relieved: fewer rooms meant fewer chores and more evenings outside.

Ways to Cut Costs When Moving to a Smaller Home

Even a well‑planned move can bleed money if you don’t control the small stuff. There are many practical ways to cut costs when moving to a smaller home without sliding into extreme frugality. Sell large furniture that won’t fit instead of paying to move and store it. Shift your move to off‑peak days — mid‑week and mid‑month are often cheaper. Use second‑hand boxes from local shops. Ask friends to help with part of the move, and hire professionals only for heavy items. Historically, families and communities always shared labor during moves; you’re simply reviving that old cooperative habit.

Development Tips: Turning Downsizing into an Upgrade

Think of your new, smaller place as a lab for better habits. Use the move to redesign how you live, not just where. A popular scientific view on happiness shows that experiences and autonomy bring more satisfaction than square footage. Allocate some of the monthly savings to skill‑building or health: online courses, therapy, fitness or creative hobbies. When you build your budget, create a “growth line” — a fixed amount reserved for personal development. That shifts the narrative from “I’m giving up space” to “I’m buying opportunities”, which makes strict budgeting emotionally sustainable in the long run.

Successful Cases: What Works in Practice

One 60‑year‑old teacher planned to retire at 67, but rising costs made that unrealistic. After analyzing the cost of moving to a smaller house and saving money on utilities, insurance and transport, she sold her large home and moved to a walkable neighborhood near public transit. Her moving budget included insulation upgrades and efficient appliances. Within three years, her total monthly outgoings dropped by 35%, allowing semi‑retirement at 63. Another case: a remote worker left an expensive capital city for a smaller town, using the price difference to build a solid investment portfolio instead of paying for an address.

Resources to Learn Smart Budgeting in 2025

You don’t have to build your system from scratch. Today there are specialized blogs, podcasts and courses focused on housing decisions and life design. Look for platforms that discuss both psychology and numbers, not just “minimalism aesthetics”. Many national housing agencies publish checklists and explain legal fees and tax implications in plain language. Apps for expense tracking let you tag move‑related costs and compare them with your initial plan. If possible, talk to a fee‑only financial planner experienced in relocations: they can refine your financial checklist for downsizing your home so it matches current laws and local prices.

Bringing It All Together: Your Future, Not Just Your Floor Plan

Downsizing in 2025 is happening against the backdrop of economic uncertainty, climate pressure and changing careers. That makes a move to a smaller home both a financial and a philosophical decision. When you treat it as a thoughtful project — with clear motives, a detailed budget and honest trade‑offs — you’re not “shrinking” your life, you’re editing it. History shows that housing norms change every few decades; you’re simply choosing to be ahead of the curve. Let your budget become a compass: each line item either pulls you back into old patterns or funds the life you actually want.