Understanding the Challenge of Saving on a Modest Income

Planning for retirement can feel overwhelming, especially when you’re working with a limited income. Many individuals assume that saving is only for those earning six figures, but this belief is one of the biggest obstacles to financial security later in life. While a modest income does present unique challenges, it also forces a higher level of financial discipline and prioritization — traits that often lead to better long-term outcomes than those with larger, but poorly managed, incomes.

Real-world data supports this. According to a 2023 report from the Employee Benefit Research Institute, over 40% of lower-income workers do not participate in any retirement savings plan, mainly due to the misconception that small contributions are ineffective. But the truth is, consistent saving — even in small amounts — can compound into a substantial nest egg over time.

Common Mistakes Beginner Savers Make

When people begin saving for retirement, especially on limited earnings, they often fall into predictable traps. These errors are usually based on misinformation or short-term thinking.

1. Waiting too long to start saving

Many assume they’ll “start saving when they make more.” But income tends to rise slowly, while expenses increase rapidly. Delaying even five years can dramatically reduce your retirement savings due to the lost time for compound growth.

2. Underestimating future expenses

Beginner savers often believe their retirement needs will be minimal. In reality, healthcare costs alone continue to rise. Fidelity estimates that a 65-year-old couple retiring in 2024 will need approximately $315,000 for medical expenses throughout retirement — not including housing, food, or leisure.

3. Failing to automate savings

Relying on manual transfers or leftover income leads to inconsistent saving. Without automation, it’s too easy to spend what could have been invested.

4. Ignoring employer-sponsored plans

Workers sometimes pass on 401(k) plans, especially if employer matching seems small. But even a 3% match on a $35,000 salary is over $1,000 annually — essentially free money that compounds over decades.

5. Investing too conservatively too early

Many new savers, fearing loss, park money in low-yield accounts. While caution is understandable, a 30-year-old with a 100% bond portfolio risks missing out on decades of stock market growth.

Strategy: Start Small, Grow Consistently

One of the most effective tactics for modest-income savers is the “percentage-based approach.” Instead of trying to set aside a fixed dollar amount, commit to saving a percentage — even if it’s just 5%. This scales naturally with income and keeps saving proportional.

Let’s consider a real example: Ana, a 28-year-old administrative assistant earning $38,000/year. She starts by contributing 5% of her salary to her employer’s 401(k), taking advantage of a 3% match. That’s $1,900 from her, plus $1,140 from her employer annually. Assuming a 7% average return, by age 65, Ana could have over $350,000 — built from modest, consistent contributions.

Technical Insight: The Power of Compound Growth

Compound interest is the backbone of long-term wealth building. Here’s how it works:

– Initial annual contribution: $2,500

– Average annual return: 7%

– Time invested: 35 years

With these inputs, the future value of the portfolio exceeds $370,000 — even though only $87,500 was personally contributed over time. The rest? Compound earnings.

This underscores why starting early is more critical than starting big. Time is the most powerful variable in retirement finance.

Practical Steps to Build Retirement Security

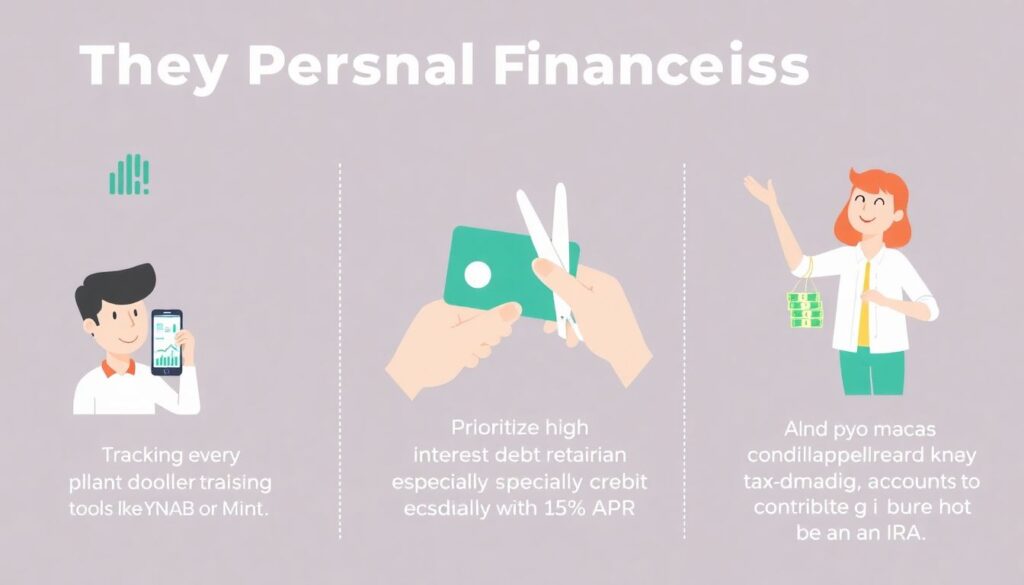

1. Track every dollar

Use tools like YNAB or Mint to monitor income and expenses. Awareness leads to better decisions.

2. Prioritize high-interest debt repayment

Eliminate credit card balances first, as 18–25% APRs will outpace any investment returns.

3. Contribute to tax-advantaged accounts

IRAs and 401(k)s lower taxable income and grow tax-free or tax-deferred, maximizing efficiency.

4. Establish a side income stream

Freelance work, gig apps, or monetizing a hobby can add hundreds monthly — reinvested into savings.

5. Reassess annually

As income grows, increase contribution percentages. Review asset allocation and adjust risk exposure according to age and goals.

Final Thoughts: Slow but Steady Wins

Saving for retirement on a modest income isn’t easy, but it is entirely achievable with a smart strategy and long-term mindset. The key is consistency, discipline, and a willingness to start — even if the numbers seem small at first. Avoiding common pitfalls and embracing simple, effective habits builds momentum. Over time, those small monthly contributions can transform into lasting financial security.